What Is Balance Sheet Reconciliation?

In financial management, the financial close is a crucial moment that marks the end of a fiscal period. However, this period comes with challenges, especially regarding balance sheet reconciliation.

This process is crucial for maintaining an organization's financial integrity, as it helps uncover any inconsistencies, omissions, or inaccuracies in the financial data presented in the balance sheet.

Financial close: process and challenges

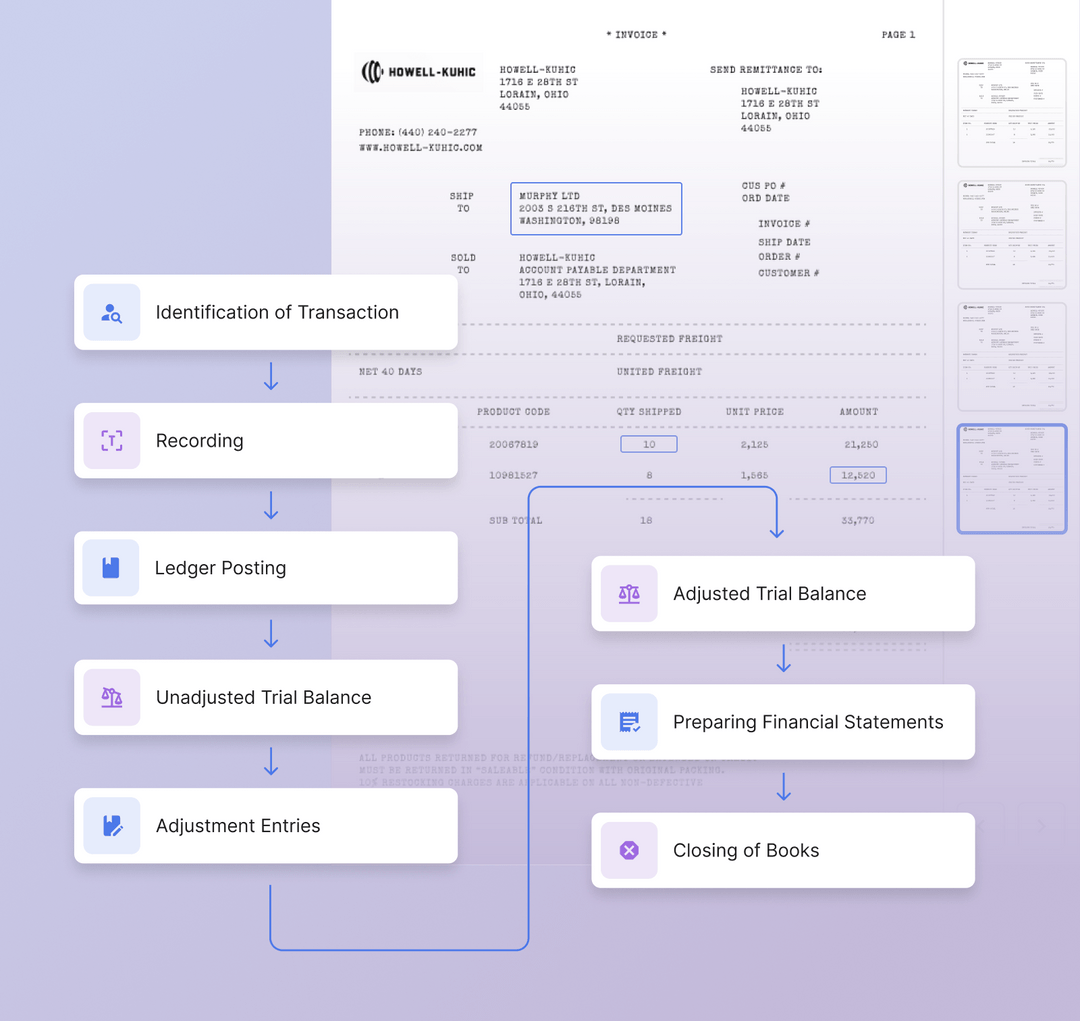

At the end of each accounting cycle, a company's accounting or finance team reviews its accounts and adjusts balances.

This is done to produce verifiable financial reports for that date. This process is known as the financial close.

What is involved in the financial close?

The financial close is typically conducted at the end of each accounting period, which may be a month, quarter, or year depending on requirements and regulatory guidelines.

The financial close process is a recurring process that ensures the accuracy and completeness of a company's financial records.

It involves collecting financial data from various departments and sources, recording adjustments and accruals, reconciling balance sheets, reviewing financial data and statements, and preparing financial statements.

The process also includes preparing documentation and records for external audits.

What are the challenges during a financial close?

During the financial close process, multiple challenges can impede efficiency and accuracy. Striving to meet deadlines set by regulatory bodies or internal reporting requirements often leads to rushed decisions and a higher risk of errors.

In the case of larger organizations, managing the substantial volume and complexity of financial data from diverse sources can be arduous. Consolidating, reconciling, and validating this data consumes significant time, potentially causing delays and errors.

Moreover, preparing for external audits to ensure audit readiness is demanding. Thoroughly organizing and documenting financial records is essential for smooth and accurate audits, placing stress on finance teams.

What is Balance Sheet Reconciliation?

Balance sheet reconciliation is an essential accounting practice that verifies the accuracy and consistency of financial statements. It involves comparing the balances of various accounts listed in the balance sheet to external documentation, such as bank statements and general ledger entries.

For a deeper dive into the intricacies of reconciling your general ledger, explore our guide on General Ledger Reconciliation, complementing your balance sheet reconciliation knowledge.

The primary purpose of balance sheet reconciliation is to identify and resolve any discrepancies or differences between the recorded balances and the supporting documentation.

This process ensures that the financial statements reflect the actual financial position of the organization and adhere to accounting standards.

Looking out for a Reconciliation Software?

Check out Nanonets Reconciliation where you can easily integrate Nanonets with your existing tools to instantly match your books and identify discrepancies.

Why is balance sheet reconciliation important in a financial close?

Several aspects of the balance sheet reconciliation make it vital to the financial close:

- Verification of transactions: Matching and verifying transactions against supporting documents and records to confirm their accuracy and completeness.

- Review of account balances: Thoroughly examine account balances to detect discrepancies between recorded figures and actual values.

- Identification of errors: Scrutinizing entries for errors, omissions, or misclassifications, ensuring that the financial statements are free from inaccuracies.

- Resolution of discrepancies: Promptly addressing any identified discrepancies, rectifying errors, and adjusting account balances as necessary.

- Compliance Validation: Ensuring compliance with accounting standards and regulations to prevent misreporting and potential legal consequences.

- Documentation: Maintaining comprehensive reconciliation process documentation and providing an audit trail for external verification.

- Supporting audits: Facilitating external audits by presenting well-reconciled and documented accounts that instill confidence in the accuracy of financial statements.

Essentially, balance sheet reconciliations are essential during the financial close as they ensure the accuracy and integrity of an organization's financial statements.

How to reconcile balance sheets?

Reconciling balance sheets is the process of comparing and matching the balances of accounts on the balance sheet with the corresponding balances in supporting documentation. This ensures that the balance sheet is accurate and complete.

To reconcile balance sheets, you can follow these steps:

Gather Documentation

Gather all relevant financial records, including bank statements, general ledger entries, and supporting documents for each account listed on the balance sheet.

Compare Balances

Compare the recorded balances in the balance sheet with the corresponding balances in the supporting documentation. This involves matching the account balances line by line and ensuring they align.

Investigate Discrepancies

If there are any discrepancies between the balance sheet and the supporting documentation, investigate the root cause of the discrepancy. Common causes of discrepancies include errors in data entry, timing differences, or missing transactions.

Resolve Issues

Once you have identified the root cause of a discrepancy, take the necessary steps to resolve it. This may involve adjusting journal entries, contacting relevant parties for clarification, or updating records to reflect accurate balances.

Document the Reconciliation

Keep clear and comprehensive documentation of the reconciliation process. This documentation should include the steps taken, findings, and any adjustments made.

It also serves as an audit trail and references future reconciliations or audits.

Balance Sheet Reconciliation: Real life Example

Balance sheet reconciliation, particularly from sub-ledger to general ledger (GL) matching, is a vital process for ensuring financial accuracy within a company. This process entails a detailed comparison of transactions listed in specific categories like accounts payable (AP), accounts receivable (AR), and fixed assets (FA) in the sub-ledgers against those recorded in the general ledger. The goal is to verify that the figures in both ledgers align, confirming the absence of discrepancies or errors.

Consider this real-life example of balance sheet reconciliation:

- General Ledger Balance: $250,000

- Adjustments:

- Addition: Revenue recognized in the sub-ledger but not reflected in the GL due to a synchronization error - $50,000

- Deduction: A discount granted to a client not updated in the GL - $20,000

- Sub-ledger Adjusted Balance: $280,000

This example illustrates a scenario where the initial comparison reveals a difference between the sub-ledger and general ledger balances. Potential reasons for such mismatches include:

- Direct manual adjustments made in the GL.

- Issues with the configuration of master data leading to incorrect GL account mappings.

- Problems with the integration between different financial systems.

Ideally, all entries in the sub-ledgers should perfectly match the corresponding entries in the general ledger, ensuring that the sum of transactions in any given sub-ledger equals the balance of its related general ledger account. However, real-world issues such as entry mistakes, timing discrepancies, or technical errors often lead to variances. Regular balance sheet reconciliation is therefore crucial for identifying and rectifying these variances, ensuring the integrity of financial reporting.

A Real-Life Balance Sheet Reconciliation Example

| Description | Amount ($) |

|---|---|

| General Ledger Balance | 250,000 |

| Add: Revenue recognized in Sub-ledger not reflected in GL due to a synchronization error | 50,000 |

| Less: Discount granted to a client not updated in GL | 20,000 |

| Sub-ledger Adjusted Balance | 280,000 |

The Costs of Manual Account Reconciliation

Balance sheet reconciliation is a crucial financial process, yet when performed manually, it can significantly hinder a company's efficiency and accuracy. The traditional approach to account reconciliation comes with several costs that can impact a business's overall performance and potential. Here are the primary drawbacks of relying on manual reconciliation methods:

- Time Consumption: Manual reconciliation involves extensive time spent on compiling, validating, and processing data through spreadsheets. This not only delays immediate tasks but also hampers the ability to engage in forward-looking business planning, forecasting, and analysis.

- Increased Expenses: While the operational costs of an accounting department vary, manual processes often result in higher expenditures. Automating reconciliation tasks can lead to substantial cost savings, allowing resources to be redirected towards strategic business support, analytics, and forecasting efforts.

- Elevated Risk: Manual accounting introduces a higher probability of errors, increasing the risk of inaccuracies in financial statements and the potential for fraudulent activities, thereby compromising the financial integrity of the organization.

- Audit and Compliance Challenges: Regulatory compliance and audit preparations are critical yet complex tasks. Manual reconciliation processes can obscure visibility and control, leading to inefficiencies, potential non-compliance, and additional costs associated with audit activities.

- Impact on Workforce Morale: Relying on manual processes can negatively affect staff morale and productivity. In contrast, accountants who leverage technology for reconciliation tasks often experience higher job satisfaction and are able to contribute more effectively to value-added activities.

In summary, the traditional manual approach to balance sheet reconciliation carries significant time and cost implications, introduces risks, complicates compliance efforts, and can demoralize talent. Embracing technological solutions for account reconciliation can mitigate these issues, enhancing efficiency, accuracy, and overall business potential.

Looking out for a Reconciliation Software?

Check out Nanonets Reconciliation where you can easily integrate Nanonets with your existing tools to instantly match your books and identify discrepancies.

Challenges of traditional balance sheet reconciliation

Traditional balance sheet reconciliation presents many challenges and pitfalls to the accuracy and effectiveness of the process. Humans are prone to typographical errors, transpositions, and other unintentional mistakes that can introduce inaccuracies into the reconciled balances.

The use of spreadsheets for reconciliation introduces vulnerabilities of its own. From version control issues to formula errors and limited collaborative capabilities, spreadsheets can inadvertently contribute to discrepancies, leading to problems in the reconciliation process.

One of the significant drawbacks of traditional methods is the need for real-time visibility into data. This deficiency delays the identification of discrepancies, making it challenging to address them promptly and make informed decisions based on accurate financial insights.

Insufficient documentation also emerges as a concern. If the reconciliation process lacks comprehensive and well-documented explanations, auditors may struggle to grasp the intricacies of the process, potentially raising doubts about the accuracy of reported figures.

As organizations grow, manual reconciliation's scalability becomes a challenge. The increasing volume and complexity of transactions can overwhelm manual processes, resulting in inefficiencies and an elevated risk of errors.

The cost of discovering errors post-finalization of financial statements can be substantial. Rectifying mistakes after the fact is time-consuming and costly, potentially tarnishing the organization's reputation and financial credibility.

Looking to automate your manual AP Processes? Book a 30-min live demo to see how Nanonets can help your team implement end-to-end AP automation.

Balance sheet reconciliation best practices

The balance sheet is one of the three primary financial statements, and it provides a snapshot of your company's assets, liabilities, and equity at a specific time. It is essential to maintain it efficiently.

Here are some best practices for preparing a balance sheet:

- Use a consistent format and terminology. This will make it easier to compare the balance sheet over time and to other companies.

- Be accurate and complete. The balance sheet should reflect all of the company's assets, liabilities, and equity at the reporting date.

- Use appropriate valuation methods. The assets and liabilities on the balance sheet should be valued by generally accepted accounting principles (GAAP).

- Use reliable accounting software. This can help you to automate the process and reduce the risk of errors.

- Delegate responsibilities. Assign specific tasks to different individuals or teams to ensure the process is completed accurately and efficiently.

- Review the balance sheet regularly. The balance sheet should be reviewed regularly to identify any potential problems or errors.

Following these best practices ensures that your balance sheet is accurate, complete, and valuable.

How automation improves balance sheet reconciliation

With technological advancements, the conventional challenges associated with balance sheet reconciliation are being met with a transformative solution: automation.

Automation enhances the balance sheet reconciliation process's accuracy, efficiency, and effectiveness.

Here are some of the ways that automation can improve the balance sheet reconciliation process:

- Data extraction: Automation can extract data from bank statements, invoices, and other supporting documents. This eliminates the need for manual data entry, which can save time and reduce errors.

- Data comparison: Automation can be used to compare the extracted data with the balances on the balance sheet. This can help to identify discrepancies quickly and efficiently so that they can be investigated and resolved promptly.

- Audit trail: Automation can create an audit trail of the reconciliation process. This provides a record of the steps that were taken and the decisions that were made. This can help to improve accountability and prevent fraud.

- Reporting: Automation can be used to generate reports on the reconciliation process. These reports can be used to track the reconciliation process's progress and identify improvement areas.

Automation can help to improve the balance sheet reconciliation process in several ways. It can help to reduce the risk of errors by automating the data entry and comparison process.

It can also improve efficiency by freeing accountants to focus on other tasks, such as analysis and reporting. Additionally, automation can help businesses to comply with regulations by creating an audit trail of the reconciliation process.

Finally, automation can increase visibility into financial data by giving businesses greater insights into their financial performance.

How can Nanonets help streamline your balance sheet reconciliations?

Nanonets is an AI-powered solution that can streamline and automate the balance sheet account reconciliation process.

It uses OCR technology to extract data from bank statements and other documents and then compares the extracted data to the recorded balances on the balance sheet.

This helps to identify discrepancies quickly and efficiently to resolve them promptly. Nanonets also maintains an audit trail of the reconciliation process, which provides transparency and accountability.

Here are the key benefits of using Nanonets for balance sheet reconciliation:

- Increased efficiency: Nanonets can automate the time-consuming and error-prone task of data entry, freeing up accountants to focus on other tasks.

- Improved accuracy: Nanonets can identify discrepancies more quickly and easily than manual reconciliation, leading to more accurate financial statements.

- Enhanced control: Nanonets provides a detailed audit trail of the reconciliation process, which can help to identify and prevent fraud.

- Reduced risk: Nanonets can help reduce the risk of errors and fraud, protecting businesses from financial losses.

The future of balance sheet automation lies in automation, enabling organizations to navigate the financial close process with the highest standards of financial integrity.

FAQs

What are the 3 types of reconciliation?

The three most common types of reconciliation are bank reconciliation, account reconciliation, and balance sheet reconciliation.

How do you reconcile a trial balance on a balance sheet?

You can reconcile a trial balance on a balance sheet by comparing the balances of the accounts on the trial balance with the corresponding balances in the ledger.

What is general ledger reconciliation?

General ledger reconciliation is the process of ensuring that the balances in the general ledger agree with the balances in the supporting documents.