Cash from operating activities definition

/What is Cash from Operating Activities?

Cash from operating activities is the aggregate amount of cash flow reported in the operating activities section of the statement of cash flows of a business. This statement is part of the organization’s financial statements. Operating activities refer to the primary revenue-generating activities of an entity, such as cash received from the sale of goods or services, royalties on the use of company-owned intellectual property, commissions for sales on behalf of other entities, and cash paid to suppliers.

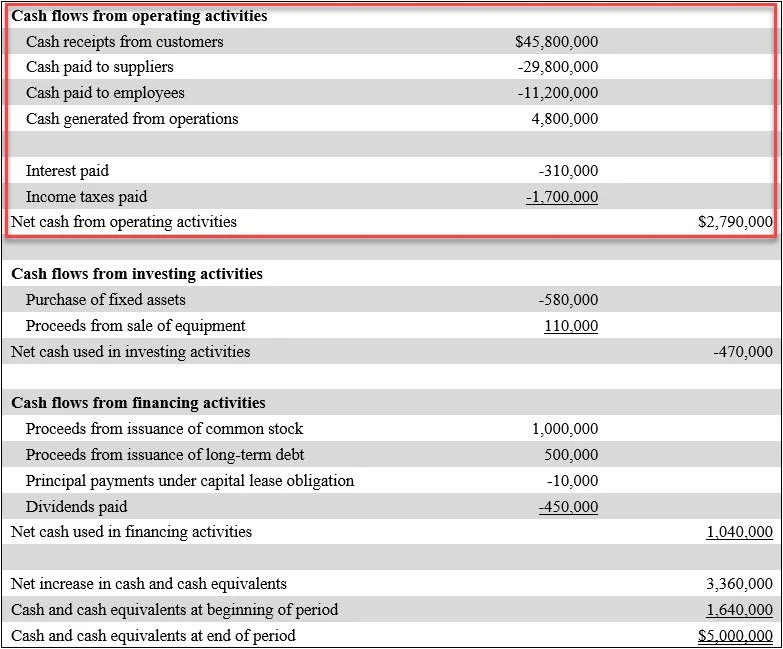

The operating activities category does not include investing activities, which are comprised of cash inflows from the liquidation of investments, or cash outflows for the purchase of new investment instruments. The operating activities category also does not include financing activities, which relate to cash flows from the issuance or repurchase of a company's own shares, the issuance of its own debt instruments, or the payout of dividends. The investing activities and financing activities are reported lower down in the statement of cash flows. A sample layout for cash from operating activities appears in the following exhibit.

Related AccountingTools Courses

The Interpretation of Financial Statements

How to Calculate Cash from Operating Activities

The amount of cash flows from operating activities can be approximately derived with the following formula:

EBIT + Depreciation = Cash from operating activities

Note: EBIT = Earnings before interest and taxes

How to Use Cash from Operating Activities

This information can be quite useful for determining how much cash the primary operations of a business are actually spinning off (if at all), which is not always apparent if you only rely on the net income figure listed in the income statement. Accrual accounting can yield a net income figure that is quite different from cash flows.