This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In this comprehensive guide, you’ll discover: The exact differences between cash, accrual, and hybrid accounting methods. It determines WHEN you recognize income and expenses on your books a seemingly small detail that creates massive ripple effects across your financial statements, tax returns, and business decisions.

Familiarize Yourself With Your Bookkeeping System Businesses use two primary methods to document revenue and expenses and report to the IRS: cash basis or accrual. Accrual Basis Bookkeeping With accrual basis bookkeeping, you record income when it’s earned and expenses when they are incurred, regardless of when money is exchanged.

Related AccountingTools Courses Closing the Books The Soft Close The Year-End Close Advantages of a Virtual Close There are several advantages associated with using a virtual close, which are as follows: Early issue detection. Any errors found must be tracked down and their underlying causes eliminated.

DIY Bookkeeping Without Proper Training Trying to manage your books without understanding basic accounting principles can be more damaging than neglecting them altogether. Failing to Reconcile Bank and Credit Card Statements Reconciliation isnt just a formalityits how you ensure your books reflect your businesss reality.

Plus, your payroll seamlessly syncs with your books. Here are some articles you might find helpful: Cash Vs. Accrual Accounting: Which Method Suits Your Small Business? Our team handles everythingfrom employee payments to tax deposits and filings. We manage compliance deadlines, calculate withholdings, and ensure timely payments.

TAX CANDIDATES FTE Senior Tax Accountant | Candidate ID #23560436 Certifications: EA in process Education: BBA Accounting Experience (years): 7+ years in public accounting Work experience (detail): Tax manager with a CPA firm Client account clean up Prepared 500+ returns in 2024 tax season Reviewed 200+ returns Client niches: Manufacturing, Hospitality, (..)

Blake and David examine the mysteries and motives surrounding the recent Macy's accounting scandal, where a single employee allegedly concealed $132-154 million through improper accrual entries. Let the listeners of The Accounting Podcast know by running a classified ad.

What is an Accrual? An accrual allows a business to record expenses and revenues for which it expects to expend cash or receive cash, respectively, in a future period. It is an essential element of the accrual basis of accounting. Where Do Accruals Appear on the Balance Sheet?

However, it may be necessary to convert to the accrual basis of accounting , perhaps to have the company's books audited in preparation for its sale, or to go public, or to obtain a loan. The accrual basis is used to record revenues and expenses in the period when they are earned, irrespective of actual cash flows.

As an accounting professional, you may have been trained to use journal entries liberally (I know I was), but in QBO there are some situations where journal entries help, and some where they can really mess up the books ! I’ll share my tips and best practices for using journal entries in a QBO cleanup without messing up the books.

Accrued expenses, also known as accrued liabilities, refer to expenses that are recognized on the books before they have been paid. The expense is recorded during the period in which it is incurred, rather than when it is paid.

Related Courses Bookkeeper Education Bundle Bookkeeping Guidebook What is the Accruals Concept in Accounting? An accrual is a journal entry that is used to recognize revenues and expenses that have been earned or consumed, respectively, and for which the related cash amounts have not yet been received or paid out. Sales accrual.

What is an Over Accrual? An over accrual is a situation where the estimate for an accrual journal entry is too high. This estimate may apply to an accrual of revenue or expense. Thus: If there is an over accrual of $500 of revenue in January, then revenue will be too low by $500 in February.

Related Courses Bookkeeping Guidebook Closing the Books The Year-End Close What is an Under Accrual? An under accrual is a situation in which the estimated amount of an accrual journal entry is too low. This scenario can arise for an accrual of either revenue or expense.

Related Courses Accountants’ Guidebook Bookkeeper Education Bundle Bookkeeping Guidebook What is Accrual Accounting? Accrual accounting is the recording of revenue when earned and expenses when incurred. Accrual accounting results in the most accurate picture of how well a business is actually performing.

Related Courses Closing the Books The Soft Close The Year-End Close What is a Soft Close? A soft close is defined as closing the books using an abbreviated closing procedure. Or, they may have more variable results from month to month because accruals are not being used to smooth out reported results over multiple reporting periods.

Related Courses Closing the Books The Year-End Close The Soft Close What is an Accrual-Type Adjusting Entry? An accrual-type adjusting entry is a journal entry recorded at the end of a reporting period that alters the amount of revenues or expenses recorded in the income statement.

Related Courses Bookkeeper Education Bundle Bookkeeping Guidebook Reasons for Monthly AccrualsAccruals allow a business to record expenses and revenues for which it expects to expend cash or receive cash, respectively, in a future period. Related Articles The Difference Between Accruals and Deferrals What Is an Over Accrual?

Related Courses Closing the Books The Soft Close The Year-End Close What are Year-End Adjustments? Year-end adjustments are journal entries made to various general ledger accounts at the end of the fiscal year , to create a set of books that is in compliance with the applicable accounting framework.

This answer can vary depending on whether the company’s books are kept on a cash basis or accrual basis, but the general premise is the same. For accrual basis financials there are many more cashflow issues that can make it difficult to determine how much cash is available without reviewing and understanding the cashflow statement.

Multiply the ending number of accrued vacation hours by the employee's hourly wage rate to arrive at the correct accrual that should be on the company's books. If the amount already accrued for the employee from the preceding period is lower than the correct accrual , then record the difference as an addition to the accrued liability.

An alternative method for recording transactions is the accrual basis of accounting , under which revenue is recorded when earned and expenses are recorded when liabilities are incurred or assets consumed, irrespective of any inflows or outflows of cash. The accrual basis is most commonly used by larger businesses.

The choice between accrual cash-based accounting methods significantly influences financial reporting. The post Balancing the Books: A Bookkeeping Firm’s Guide to Franchise Financials appeared first on Bookkeeping Express.

The choice between accrual cash-based accounting methods significantly influences financial reporting. The post Balancing the Books: A Bookkeeping Firm’s Guide to Franchise Financials appeared first on Bookkeeping Express.

It is commonly used in situations when either revenue or expenses were accrued in the preceding period, and the accountant does not want the accruals to remain in the accounting system for another period. The reversing entry typically occurs at the beginning of an accounting period. Conduct account reconciliations.

Although many of the terms are self-explanatory, others such as bookings vs billings vs revenue are frequently misunderstood and used interchangeably. Cutting Through Financial Jargon What exactly are bookings vs billings vs revenue? Let’s start with the definition of each.

This decouples the timing of when usage is paid for from when it’s consumed, which for customers using accrual vs. cash accounting (most large companies), results in a need to amortize the prepayment. Multiple enterprise customers, currently using this feature in beta, rely on it to close their monthly books.

Related Courses Bookkeeping Guidebook Closing the Books New Controller Guidebook What are Accounting Adjustments? The adjustments are primarily used under the accrual basis of accounting. An accounting adjustment is a business transaction that has not yet been included in the accounting records of a business as of a specific date.

Accrued revenue is a cornerstone of accrual accounting, playing a vital role in accurately reflecting a company’s financial performance. What is Revenue Accrual? Revenue accrual is a key principle in accounting that ensures revenue is recognized when earned , not necessarily when cash is received.

So once you catch up on your books, continue to reconcile your bank statements each month. There may be circumstances where you need to manually adjust entries to account for accruals, depreciation, or amortization. Adjust entries Next up on the bookkeeping cleanup checklist: adjusting entries.

Practical Application of Accrued Expenses Realistically, the amount of an expense accrual is only an estimate, and so is likely to be somewhat different from the amount of the supplier invoice that arrives at a later date. Income taxes are typically retained as accrued expenses until paid, which may be at the end of a quarter or year.

Who Should (and Shouldn’t) Use Excel to Track Their Books If you’re a small business owner looking to streamline your financial tracking process (or that of your client), you may consider both Excel and QuickBooks options. However, it’s not always a smooth process with Excel templates.

Related Courses Bookkeeper Education Bundle Bookkeeping Guidebook Closing the Books Posting in accounting is when the balances in subledgers and the general journal are shifted into the general ledger. Posting is also used when a parent company maintains separate sets of books for each of its subsidiary companies.

This type of accounting entry is used under both the accrual basis and cash basis of accounting. This type of accounting entry is used under the accrual basis of accounting. If you are creating an adjusting accounting entry, then you will use a journal entry format (assuming that a double entry accounting system is being used).

The two primary accounting methods are cash accounting and accrual accounting. Hybrid accounting, as the name implies, is a mixture of cash and accrual accounting. Public corporations in the United States must use the accrual accounting method (as most corporations average more than $26 million in total yearly revenue).

The two primary accounting methods are cash accounting and accrual accounting. Hybrid accounting, as the name implies, is a mixture of cash and accrual accounting. Public corporations in the United States must use the accrual accounting method (as most corporations average more than $26 million in total yearly revenue).

Related Courses Closing the Books The Soft Close The Year-End Close What are Closing Entries? Example of Closing Entries ABC International is closing its books for the most recent reporting period. Temporary accounts are used to accumulate income statement activity during a reporting period.

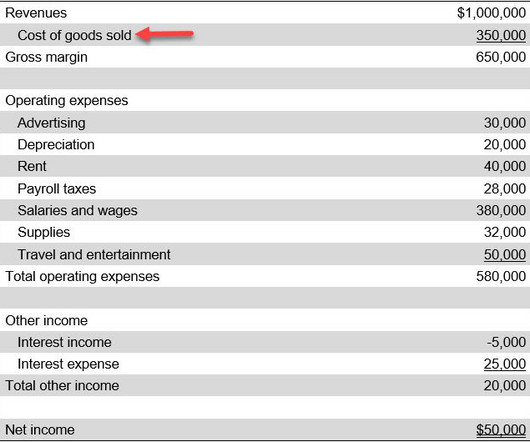

If there is a physical inventory count that does not match the book balance of the ending inventory, then the difference must be charged to the cost of goods sold. The cost of goods sold does not include any administrative or selling expenses. In addition, the cost of goods sold calculation must factor in the ending inventory balance.

Related AccountingTools Courses Auditing State and Local Governments Governmental Accounting The Green Book Explained The Yellow Book Explained The Basis of Accounting The accrual basis of accounting is adjusted when dealing with governmental funds. The sum total of these adjustments is referred to as the modified accrual basis.

Cash vs. Accrual Accounting Cash accounting records transactions only when cash changes hands, providing a real-time view of cash flow. In contrast, accrual accounting records transactions when they occur, offering a more accurate depiction of the company’s financial position over time by matching revenues with expenses.

Cash management, accounts receivable, prepaid expenses, fixed assets, accounts payable – there are countless activities that must be accounted for before closing the books for the month. You can track the status of any invoice at any time, giving you the ability to analyze critical metrics like approval cycle times and month-end accruals.

Related Courses Bookkeeping Guidebook Closing the Books The Year-End Close What is an Unadjusted Trial Balance? The unadjusted trial balance is the listing of general ledger account balances at the end of a reporting period, before any adjusting entries are made to the balances to create financial statements.

Otherwise, someone reviewing the books at a later date will have no idea why the entry was created. Use an automatically reversing journal entry for accruals whose impact is intended to be for a single accounting period. Do not include too many line items. Use a transaction module instead of a manual journal entry.

Related Courses Bookkeeper Education Bundle Bookkeeping Guidebook Closing the Books What are the Steps in the Accounting Process? The third group is the period-end processing required to close the books and produce financial statements. This information is then aggregated into financial statements.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content