This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

What is the Accrual Basis of Accounting? The accrual basis of accounting is the concept of recording revenues when earned and expenses as incurred. The accrual basis of accounting is advocated under both generally accepted accounting principles ( GAAP ) and international financial reporting standards ( IFRS ).

Related Courses Bookkeeping Guidebook Human Resources Guidebook Payroll Management Accounting for a Bonus Accrual A bonus expense should be accrued whenever there is an expectation that the financial or operational performance of a company at least equals the performance levels required in any active bonus plans.

Related Courses How to Audit Payroll Optimal Accounting for Payroll Payroll Management What is a Wage Accrual? The accrual entry shown below is a simple one, because you typically clump all payroll taxes into a single expense account and offsetting liability account.

If an entity is recording its business transactions under the accrual basis of accounting , it is quite possible that the profitability condition will not be matched by the cash flows generated by the organization, since some accrual-basis transactions (such as depreciation ) do not involve cash flows.

An alternative method for recording transactions is the accrual basis of accounting , under which revenue is recorded when earned and expenses are recorded when liabilities are incurred or assets consumed, irrespective of any inflows or outflows of cash. The accrual basis is most commonly used by larger businesses. Ease of use.

Income taxes are accrued based on income earned. Debit to income tax expense, credit to accrued expenses. Income taxes are typically retained as accrued expenses until paid, which may be at the end of a quarter or year. The first three entries should reverse in the following month.

This is used to determine the amount of earnings generated in a reporting period, net of income taxes. If the accrual basis of accounting is used, this can result in a figure that is different from what cash flows would indicate, due to the accrual of expenses for which payments have not yet been made.

For example, you could accrue unpaid wages at month-end if the company is on the accrual basis of accounting. For example, the journal entry to record payroll usually contains many lines, since it involves the recordation of numerous tax liabilities and payroll deductions.

Related Courses Human Resources Guidebook Optimal Accounting for Payroll Payroll Management Understanding the Common Paymaster Concept When a parent company owns a number of subsidiaries , the company as a whole may pay more payroll taxes than is strictly necessary. The same problem also arises for federal unemployment (FUTA) taxes.

Related Courses Bankruptcy Tax Guide Essentials of Corporate Bankruptcy What is the Liquidation Basis of Accounting? The Difference Between Liquidation Basis and Accrual Basis Accounting The accounting under the liquidation basis of accounting differs in several respects from normal accrual basis accounting.

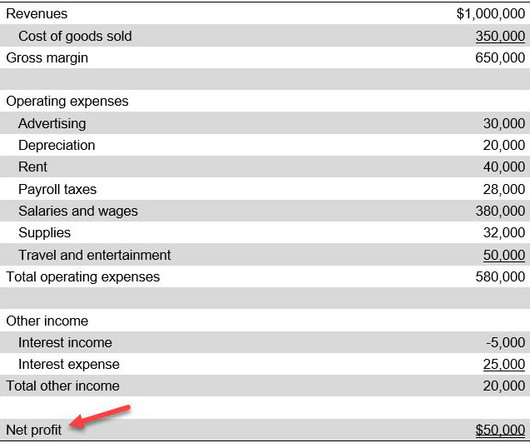

How to Calculate Net Profit To calculate net profit, subtract the cost of goods sold , operating expenses , financing costs, and tax costs from net revenues. Differences between net profit and net cash flows include timing issues related to accrual-basis accounting and the reduction of cash flows caused by expenditures for fixed assets.

What is a Tax Election? A tax election is a choice made by a taxpayer among several possible options for how to deal with a situation from a tax reporting perspective. A tax election may have consequences related to the timing and amount of taxes paid.

Here is an example section for an Accrual Bookkeeping Service. Bookkeeping Services (Accrual). These definitions are crucial to success in starting a bookkeeping business. . Example: Alpha and Beta Accounting is to take responsibility for the bookkeeping and tax preparation of ABC, Inc. Service Terms Template/Example.

The outcome of a P&L can vary, depending on whether a business is using the cash basis or accrual basis of accounting. It represents the financial outcome of the business before financing and tax issues. Income Taxes The income taxes line item contains the amount of income taxes recognized by the business for the reporting period.

If the accrual basis of accounting is used, then the amount earned will be recorded, irrespective of the amount of cash received. Under the accrual basis, you can record interest earned as long as receipt of the related amount of cash is probable, and you can reasonably estimate the amount of the payment.

Related Articles Extended Trial Balance How to Prepare a Trial Balance The Difference Between an Adjusted and Unadjusted Trial Balance The Difference Between the General Ledger and Trial Balance The Purpose of a Trial Balance Trial Balance Errors

An alternative way to calculate the cash flow of an entity is to add back all non-cash expenses (such as depreciation and amortization ) to its net after-tax profit, though this approach only approximates actual cash flows. Cash inflows come from the sources noted below.

Under the accrual method of accounting , you should charge them to expense in the period incurred. This means that selling expenses tend to be recognized as expenses more quickly under the accrual method than under the cash basis of accounting. Selling expense (or sales expense) includes any costs incurred by the sales department.

This measurement is one of the key indicators of company profitability , along with gross margin and before-tax income. How to Calculate Net Income A common calculation for net income is to subtract the cost of goods sold , administrative expenses , and income tax expense from net sales.

Creative accounting can also be used to reduce reported profit levels, typically to avoid paying taxes. Creative accounting techniques are generally acceptable under the relevant accounting framework , but operate in a gray area where reported results are definitely being skewed away from actual results.

The accrued payroll concept is only used under the accrual basis of accounting ; it is not used under the cash basis of accounting. The key components of accrued payroll are salaries , wages , commissions , bonuses, and payroll taxes. It represents a liability for the employer.

This accrual may be accompanied by an additional entry to accrue for any related payroll taxes. Related Articles Accrued Payroll Benefits Accrual Accounting Bonus Accrual How to Calculate Accrued Vacation Pay This unpaid amount is $640, which the employer should record as accrued wages as of month-end.

Final accounts is a somewhat archaic bookkeeping term that refers to the final trial balance at the end of an accounting period from which the financial statements are derived.

This accrual may be accompanied by an additional entry to accrue for any related payroll taxes. Related Articles Bonus Accrual How to Account for Unpaid Wages How to Calculate Accrued Vacation Pay How to Calculate Payroll Overtime Pay Calculation Payroll Accounting

Related Articles Accounting Journal Entries Accrual-Type Adjusting Entries Correcting Entry Deferral-Type Adjusting Entry How to Write an Accounting Journal Entry Simple Journal Entry Bookkeeping Efficiency It is more efficient from a bookkeeping perspective to aggregate the underlying business transactions into a single entry.

The Difference Between Profit and Cash Flows The resulting profit may not match the amount of cash flows generated during the same reporting period ; this is because some of the accounting transactions required under the accrual basis of accounting do not match cash flows, such as the recordation of depreciation and amortization.

Alternatively, the account contains the amount of fees actually earned during the reporting period, irrespective of the amount of cash received from customers, if the reporting entity is operating under the accrual basis of accounting.

Reversing Accruals Most accrued liabilities are created as reversing entries , so that the accounting software automatically cancels them in the following period. This accrual is recorded when a company has a loan outstanding, for which it owes interest that has not yet been billed by its lender at the end of an accounting period.

The allocation of factory burden is required when a business is generating financial statements under the accrual basis of accounting. The allocated costs are eventually charged to expense when the associated units of production are sold.

Operating profit is the income earned from the core operations of a business, excluding any financing or tax-related issues. Operating profit is stated as a subtotal on a company's income statement after all general and administrative expenses , and before the line items for interest income and interest expense , as well as income taxes.

Net income margin is the net after-tax income of a business, expressed as a percentage of sales. The net income margin formula is: Net income ÷ Sales = Net income margin Example of Net Income Margin ABC International has net after-tax income of $50,000 and sales of $1,000,000.

Payroll accounting definition Payroll accounting calculates, distributes, and tracks employees’ compensation. These regulatory agencies control the amount of taxes withheld, how benefits and garnishments are paid and record retention requirements. Payroll accounting follows the matching principle under accrual accounting.

EBITDA is a contraction of earnings before interest, taxes, depreciation , and amortization. The interest and tax line items that are excluded from the measure are not directly related to company operations, while the depreciation and amortization line items are non-cash items.

Related Courses Small Business Tax Guide What is the Cash Method of Accounting? Limitations on Use of the Cash Method Given the tax advantages of the cash method, the IRS restricts its use with the following rules: It is not allowed for C corporations or tax shelters.

The name is a contraction of the term Earnings Before Interest, Taxes, Depreciation, and Amortization. How to Calculate EBITDA The formula for EBITDA is to add back to a firm’s earnings its interest, taxes, depreciation, and amortization.

Thus, a business might never report an extraordinary item. If extraordinary items were reported on the income statement, then earnings per share information for the extraordinary items were to be presented either in the income statement or in the accompanying notes.

Examples of other fixed costs are insurance, depreciation , and property taxes. Allocation of Fixed Costs Fixed costs are allocated under the accrual basis of cost accounting. Fixed costs tend to be incurred on a regular basis, and so are considered to be period costs.

And, so, a lot of this stuff we're just starting to figure out right now. Definitely, in the accounting side, we're starting to see some use cases for coding transactions and things like that. I think it's going to definitely change the accounting side, the day-to-day transactional stuff. But I think it'll make us more efficient.

In essence, then, profit is calculated using the accrual basis of accounting , not the cash basis. Related Articles After-Tax Real Rate of Return How to Calculate the Internal Rate of Return Incremental Internal Rate of Return Internal Rate of Return The Effective Rate of Return The Simple Rate of Return

A cleanup starts with your client’s messy or incomplete books and follows a process – which includes reviewing the books, catching them up, fixing problems, and reconciling – and ends with books that are complete, accurate, and tax-ready. Tax form that’s being filed ( depends based on entity type and location).

Problems with the Net Income Formula The results of the net income formula may not be reliable, since management may fraudulently twist the rules of accrual basis accounting to modify the reported profit. The reverse situation can also occur, where the net profit figure is artificially reduced in order to avoid paying income taxes.

These frameworks mandate the use of accrual basis accounting in deriving the accounting profit figure. Examples of accounting frameworks are Generally Accepted Accounting Principles ( GAAP ) and International Financial Reporting Standards ( IFRS ). Accounting Profit vs.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content