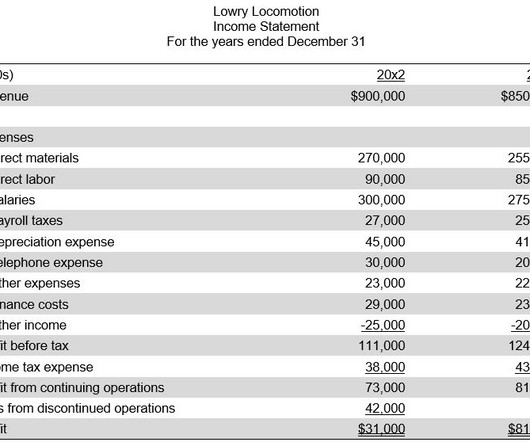

Recognized loss definition

Accounting Tools

APRIL 12, 2024

What is a Recognized Loss? A recognized loss occurs when an asset is sold for an amount less than its purchase price. Recognized losses can be incorporated into tax planning. Example of a Recognized Loss Alyssa purchased a rental property several years ago as an investment, paying $400,000 for it.

Let's personalize your content