This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The eCommerce accounting services guarantee international sales are accurately recorded in your books. The best eCommerce accounting services reconcile your platform payments with real-life bank deposits and expenditures. This leads to more accurate tax filings and robust financialstatements throughout the year.

It determines WHEN you recognize income and expenses on your books a seemingly small detail that creates massive ripple effects across your financialstatements, tax returns, and business decisions. Under cash basis accounting, that money doesn’t exist on your books until the payment hits your bank account in January.

Maybe you just want someone to handle your monthly books. Or perhaps you need a complete financial team including CFO to improve cash flow management. Bookkeeping Services Bookkeeping serves as the foundation of your financial management system, and it’s one of the most outsourced accounting functions.

These systems can track income and expenses, generate financial reports, and integrate with other financial tools, ensuring accuracy and efficiency. Regularly Reconcile Accounts Reconciling accounts involves comparing financial records with bank statements to ensure they match.

Types of Accounting Services and Their Cost Factors The cost of accounting services largely depends on what you need from basic bookkeeping to comprehensive financial management. Bookkeeping Typically charged monthly or quarterly, bookkeeping services involve recording daily transactions, reconciling bank statements, and maintaining ledgers.

Outsourced bookkeeping services entail a process to maintain financial records beyond the physical office setting. Instead of hiring only one or two employees to take care of every task, like reconciliation, accounts payable, financialstatement generation, and so on, you can hire a whole company.

Accurate Reporting and GAAP Compliance In business activities, proper financial reporting needs to be done especially where there are lenders or stakeholders. They further uphold ledger book integrity and discharge account administration duties including receivables, payables, and monthly bank reconciliation. Yes, of course.

Related Courses Closing the Books The Soft Close The Year-End Close How to Prepare FinancialStatements The preparation of financialstatements involves the process of aggregating accounting information into a standardized set of financials. Accrue the expense for any invoices that have not been received.

When a person is reconciling the general ledger, this usually means that individual accounts within the general ledger are being reviewed to ensure that the source documents match the balances shown in each account. If the account has not been reconciled for some time, it is possible that the error lies several periods in the past.

Bank Reconciliation Vs. Book Reconciliation In accounting and financial management, we encounter the terms "Book Reconciliation" and " Bank Reconciliation " These terms are often used interchangeably, leading to ambiguity regarding their meanings. What Is Book Reconciliation?

Related Courses Accountants’ Guidebook Bookkeeper Education Bundle Bookkeeping Guidebook What are Books of Original Entry? Books of original entry refers to the accounting journals in which business transactions are initially recorded. Terms Similar to Books of Original Entry A journal may also be referred to as a day book.

FinancialStatements and Analysis 1. Review FinancialStatements Take a look at your “big three” accounting reports: income statement, balance sheet, and cash flow statement for accuracy. It will also give you a great picture of your business’s overall financial health.

Presentation of Ledger Accounts The information in a ledger account is summarized into the account-level totals shown in the trial balance report, which in turn is used to compile financialstatements. Terms Similar to Ledger Account A ledger account is also known as an account.

Related Courses Closing the Books The Soft Close The Year-End Close What are Year-End Adjustments? Year-end adjustments are journal entries made to various general ledger accounts at the end of the fiscal year , to create a set of books that is in compliance with the applicable accounting framework.

Related Courses Accountants' Guidebook Bookkeeping Guidebook New Controller Guidebook An accountant is a person who records business transactions on behalf of an organization, reports on company performance to management, and issues financialstatements. Management reports are issued to the management team.

Who Should (and Shouldn’t) Use Excel to Track Their Books If you’re a small business owner looking to streamline your financial tracking process (or that of your client), you may consider both Excel and QuickBooks options. Run financial reports and data analytics easily. Track, reconcile, and manage inventory.

Reconcile bank statements The next step in your bookkeeping cleanup checklist is to reconcile your bank statements. Take a look at your bank statements over the course of the timeframe you are working on. So once you catch up on your books, continue to reconcile your bank statements each month.

By maintaining your books regularly, reviewing reports, and reconciling your accounts at the end of each month, you can avoid bookkeeping disasters. Finally, having clean books simplifies making wise business choices and helps you stay organized for tax season. Are you looking for someone to manage your books?

A balance sheet is a financialstatement that provides a snapshot of a company's financial position at a specific point in time. Balance sheet reconciliation is a critical financial process that aligns the financialstatements with external documentation such as bank statements, invoices, and general ledger entries.

Source documents are typically retained for use as evidence when auditors later review a company's financialstatements , and need to verify that transactions have, in fact, occurred. Examples of Source Documents Examples of source documents, and their related business transactions that appear in the financial records, are noted below.

During this process, you’ll reconcile transactions with accounts, categorize transactions for analysis and tax purposes, and handle any employee or vendor reimbursements. Financial reporting and forecasting: You will typically provide the company’s management team with regular financial reports, financial forecasts, and more.

Manually reconciling bank statements. Producing financial reports in a spreadsheet. Before the books are closed, it’s typical for senior accountants to review the books to spot any accounting errors or potential issues. to prepare their financialstatements. Paying suppliers one-by-one. Easy peasy!

Understanding accrued revenue meaning is essential because it aligns a companys financialstatements with the business’s actual performance. Before closing the books for August, the business records the earned revenue as accrued revenue, ensuring accurate reporting for the period.

Traditional bookkeepers are professionals responsible for recording financial transactions, maintaining ledgers, and preparing financialstatements manually or using basic accounting software. These professionals play a crucial role in ensuring the accuracy and integrity of a company's financial records.

Introduction Diving into the world of accounting, reconciling accounts becomes a routine yet crucial task, especially when bank or credit card statements roll in. However, the dynamic nature of business means changes or oversights can occur, necessitating a revisit to previously reconciled accounts. The answer is a Yes.

Matching and validating entries would mean data consolidation across sub-ledgers, vendor invoices, bank statements, receipts, and account receivables to ensure timely and accurate month-end and year-end closing of the financialbooks. Account Reconciliation can be a fairly manual task, especially right before the monthly close.

Review FinancialStatements Begin by reviewing your balance sheet, income statement, and cash flow statement. Analyze your company’s financial health, track profitability, and identify areas that need improvement. Reconcile Bank Accounts Ensure your bank statements align with your accounting records.

Review and Adjust FinancialStatements At the annual close, you need to thoroughly review the financialstatements prepared by your bookkeeping team against the client’s general ledger accounts. This review includes the balance sheet, income statement, and cash flow statement.

It involves the comparison between the company’s internal financial records and those of the bank. At the heart of this reconciliation lies the creation of journal entries, which serve to align discrepancies between the company's books and the bank statement.

As part of their year-end audit procedures , auditors may trace transactions from a subledger to the general ledger and from there to the financialstatements , to ensure that transactions are being recorded properly in the accounting system. Ending balance usage. Number of ledgers.

Dancing Queen" by ABBA - When the financialstatements are balanced, and you're ready to dance your way through tax season like a true queen of numbers. The Gambler" by Kenny Rogers - A reminder to always play the odds and make smart financial decisions, especially when it comes to taxes!

But if the amount is not applied to an invoice or deducted from their total outstanding balance, this can lead to a negative account balance in your books. If there is no way to reconcile this amount with another invoice or account, it can lead to a negative A/R balance. For example, a customer might choose to pay when he orders.

To address this issue, organizations prefer using reconciliation software, which can automate the heavy lifting and monotonous tasks while ensuring accuracy and timeliness during the monthly book-closing period. If Pricing is an issue you may try to use Power Query to reconcile in excel. Why do you need to do it?

Updating Internal Records and Bank Statement: Ensuring internal records align with the reconciled figures, facilitating accurate financial reporting, audit compliance, cash flow management, and fraud detection. This accuracy is crucial for understanding the financial health of the business and making informed decisions.

What are financialstatements, and how do I get them? Book a personalized live demo to see how you can save time, effort, and costs while automating your bookkeeping processes. She closes out the accounts at the end of the month and balances the books. Now you may need to know: what is bookkeeping?

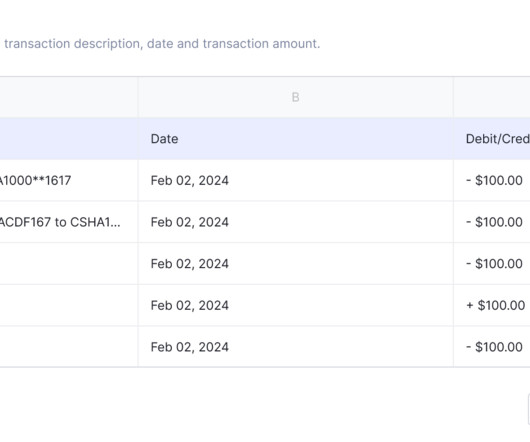

Check out Nanonets Reconciliation where you can easily integrate Nanonets with your existing tools to instantly match your books and identify discrepancies. Reconciling Items : Any differences between the adjusted bank balance and the adjusted internal balance are listed as reconciling items.

Integrate Nanonets Reconcilefinancialstatements in minutes Try for Free What is Accounts Reconciliation? At its core, account reconciliation is the comparison of multiple sets of financial records, such as bank statements and internal accounting records, to identify and rectify discrepancies.

Want to see the scary truth of neglecting your books? (Or Set aside dedicated time each week or month to update your financial records, reconcile accounts, and review financialstatements. They live and breathe numbers, spreadsheets, and financialstatements.

The general ledger, in turn, is used to aggregate information into the financialstatements of a business; this can be done automatically with accounting software, or by manually compiling financialstatements from the information in a trial balance report (which is a summarization of the ending balances in the general ledger).

This last-minute scramble typically involves gathering scattered receipts, invoices, and financialstatements, reconciling accounts, calculating tax obligations, and preparing financialstatements for tax filing. Prompt invoicing and diligent follow-up can improve cash flow and reduce financial stress.

Reconcile Cash and Receipts At the end of each day, reconcile all cash payments and payment receipts received in the general ledger to get a good idea of each client’s cash balance. Reconciling these accounts with month-end data gives you a real-time view of a client’s cash balance.

Essential Insights: Purpose : The core objective of cash reconciliation is to identify mismatches between the cash on hand and the sales transactions recorded, thereby safeguarding against financial inaccuracies in a company's records. Signing, dating the form, and submitting it for supervisory review and approval.

The role of payment reconciliation in maintaining financial accuracy is critical, as it helps businesses track their income, verify the legitimacy of transactions and prevent discrepancies. Accurate financial records are essential for businesses to meet auditing requirements and avoid potential fines or penalties for non-compliance.

To ensure a smooth process, your year-end bookkeeping functions should follow these fundamental steps to prepare for taxes: Reconcile All Accounts: Check that your bank accounts, credit cards, and loans correspond to the entries in your financial records. Adjust Journal Entries: Update your books to show asset wear and tear.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content