This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

What are FinancialStatements? Financialstatements are a collection of summary-level reports about an organization's financial results, financial position , and cash flows. They include the income statement, balance sheet, and statement of cash flows. Inaccurate basis for forecasts.

What are General Purpose FinancialStatements? General purpose financialstatements are those financialstatements released to a broad group of users. These statements include the following: Income statement. Who Receives General Purpose FinancialStatements?

Other comprehensive income is designed to give the reader of a company's financialstatements a more comprehensive view of the financial status of the entity, though in practice it is possible that it introduces too much complexity to the income statement.

What is Tax Accounting? Tax accounting refers to the rules used to generate tax assets and liabilities in the accounting records of a business or individual. Tax accounting is derived from the Internal Revenue Code (IRC), rather than one of the accounting frameworks , such as GAAP or IFRS. Future years.

Related Courses Small Business Tax Guide What is a Depreciation Tax Shield? A depreciation tax shield is a tax reduction technique under which depreciation expense is subtracted from taxable income. The tax shield concept may not apply in some government jurisdictions where depreciation is not allowed as a tax deduction.

Disclosure of a Contingent Gain If a contingency may result in a gain, it is allowable to disclose the nature of the contingency in the notes accompanying the financialstatements. However, the disclosure should not make any potentially misleading statements about the likelihood of realization of the contingent gain.

Related Courses Accounting for Income Taxes What is an Intraperiod Tax Allocation? An intraperiod tax allocation is the allocation of income taxes to different parts of the results appearing in the income statement of a business, so that some line items are stated net of tax.

Related Courses The Balance Sheet The Income Statement The Statement of Cash Flows What is a Special-Purpose FinancialStatement? A special-purpose financialstatement is a financial report that is intended for presentation to a limited group of users.

Public accountants provide accounting expertise, auditing, and tax services to their clients. FinancialStatement Preparation Personnel assist clients with the direct preparation of their financialstatements. FinancialStatement Auditing This involves auditing the financialstatements of clients.

Otherwise, the loan might instead be considered an investment by the issuing business unit in the receiving unit, which can create other tax problems. Given the extent of these tax concerns, a company using intercompany loans should be prepared to undergo a tax audit that focuses on the underlying reasons for and documentation of these loans.

As part of the billing process, the bookkeeper also remits sales taxes to the government. The bookkeeper also prepares paychecks for employees, and remits payroll taxes to the government. FinancialStatements The bookkeeper may prepare preliminary financialstatements , but may rely upon an accountant to produce the final statements.

Related Courses The Balance Sheet The Income Statement The Interpretation of FinancialStatements What is a Profit and Loss Statement? A profit and loss statement aggregates the revenues , expenses , and profits or losses of a business.

The method is commonly used to record financial results for tax purposes, since a business can accelerate some payments in order to reduce its taxable profits , thereby deferring its tax liability. Audited financialstatements. Ease of use. Management reporting.

The first is a correction of an error in the financialstatements that was reported for a prior period. The second type of prior period adjustment was caused by the realization of the income tax benefits arising from the operating losses of purchased subsidiaries before they were acquired.

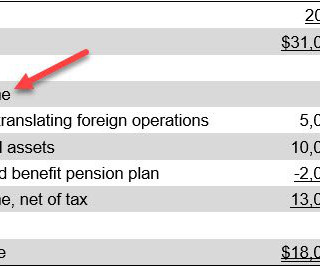

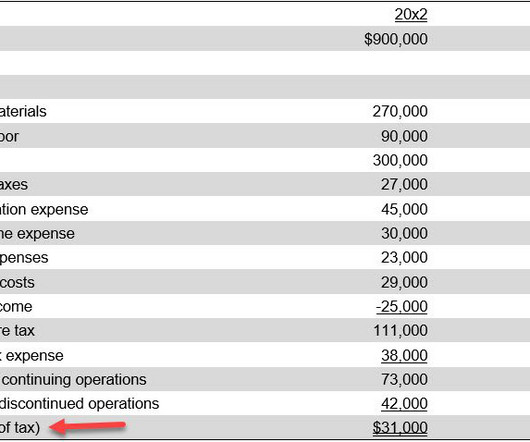

What is Net of Tax? Net of tax is the initial (or gross) results of a transaction or group of transactions, minus the related income taxes. A sample presentation of this term in an income statement appears in the following exhibit. Several variations on the net of tax concept are noted below: Accounting requirements.

The unadjusted trial balance is the listing of general ledger account balances at the end of a reporting period, before any adjusting entries are made to the balances to create financialstatements. The unadjusted trial balance is used as the starting point for analyzing account balances and making adjusting entries.

An entity may also be required to submit tax returns and pay governments for their income earned. Accounting for an Entity In accounting, transactions are recorded and financialstatements are produced for a specific entity.

As a CPA, you may also perform the following duties: Design financialstatements: CPAs usually compose documents that detail a company’s finances over time. This entails compiling financialstatements into digestible material that business owners can easily examine and use for decision-making.

There will be a reduced cost for companies once the two accounting frameworks are more closely aligned, since they will not have to pay to have their financialstatements restated to show results under the other framework in cases where they need to report their results in locations where the other framework is required.

Related Courses The Interpretation of FinancialStatements What is Profitability? The net profit ratio compares after-tax profits to revenues, while the earnings per share ratio presents profits on a per-share basis. Profitability is a situation in which an entity is generating a profit.

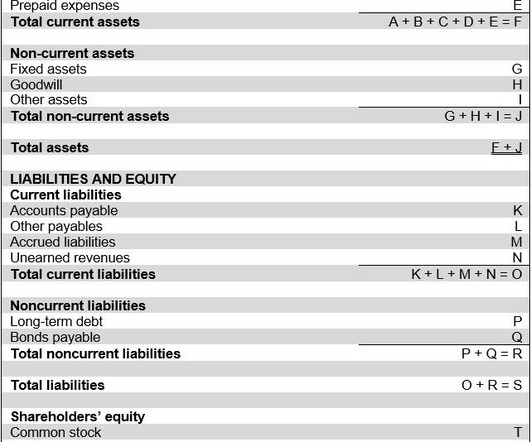

Related Courses The Balance Sheet The Interpretation of FinancialStatements What is the Statement of Financial Position? The statement of financial position is another term for the balance sheet. The statement lists the assets , liabilities , and equity of an organization as of the report date.

Deferred tax assets. These are income taxes that are recoverable in a future period. Related AccountingTools Courses The Balance Sheet The Interpretation of FinancialStatements Related Article Other Current Assets

The general ledger is then used to create financialstatements for the business. This information may be accessed by the external auditors as part of their year-end investigation of a company's financialstatements and related systems. It is frequently used to record complex transactions, or several transactions at once.

A report by Oxford University concluded that there was a 99% chance that tax preparers’ jobs would be automated and a 98% chance that it will happen to bookkeepers and accountants. to prepare their financialstatements. Here’s a good video of how MindBridge works in action: 15) Tax Planning. Over to You.

Full cycle accounting refers to the complete set of activities undertaken by an accounting department to produce financialstatements for a reporting period. Examples of Full Cycle Accounting Full cycle accounting can also refer to the complete set of transactions associated with a specific business activity.

Related Courses The Income Statement The Interpretation of FinancialStatements What is a Condensed Income Statement? A condensed income statement reduces much of the normal income statement detail to just a few lines.

Responsibilities of a Full Charge Bookkeeper The subject areas over which the full charge bookkeeper has responsibility are as follows: Record and pay accounts payable Issue invoices to and collect from customers Calculate pay and issue payments to employees Create financialstatements and related financial reports Remit payroll taxes , sales taxes (..)

MACRS depreciation is the tax depreciation system used in the United States. years A business determines its tax depreciation based on the information in the preceding table for assets ready and available for use since 1986. This can result in differences between the tax basis and book basis of an organization's fixed assets.

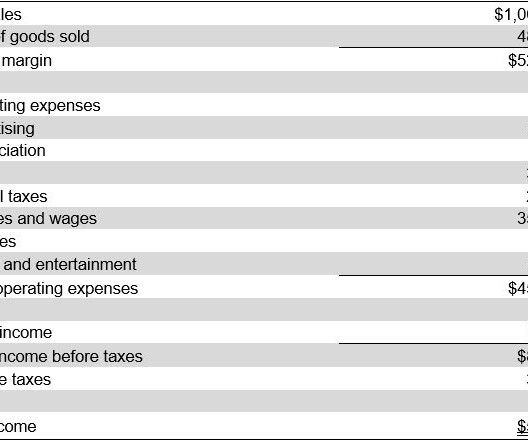

Related Courses Business Ratios Guidebook The Interpretation of FinancialStatements What is Return on Sales? An increasing return indicates an improvement in operating efficiency , while a recurring decline is a strong indicator of impending financial distress. The net sales reported for the same period is $1,000,000.

Examples of Cost of Goods Operating Expenses The definition of operating expenses is sometimes expanded to include the cost of goods sold, thereby encompassing every operational aspect of a business. Property taxes on production facilities. These expenditures are the same as selling, general and administrative expenses.

In the latter case, product cost should include all costs related to a service, such as compensation , payroll taxes , and employee benefits. Product Cost Reporting Product cost appears in the financialstatements , since it includes the factory overhead that is required by both GAAP and IFRS.

In the absence of a journal entry, the expense would not appear at all in the entity's financialstatements in the period incurred, which would result in reported profits being too high in that period. Income taxes are accrued based on income earned. Debit to income tax expense, credit to accrued expenses.

These estimates may not be entirely correct, and so can lead to materially inaccurate financialstatements. A key difference between the methods is that financialstatements produced by a business operating under the cash basis could yield results that are misleading. What is Modified Accrual Accounting?

Related Courses Business Ratios Guidebook The Interpretation of FinancialStatements What is Return on Total Assets? How to Calculate Return on Total Assets The calculation of the return on total assets is earnings before interest and taxes (EBIT), divided by the total assets figure listed on the balance sheet.

These costs are instead charged to expense as incurred; they are considered to be period expenses, and so are associated with an accounting period, rather than a product.

Although it may seem complex, this standardised format ensures efficient and transparent submission of financialstatements. Requirement: Must file financialstatements in XBRL format. XYZ Pte Ltd is required to file its financialstatements in XBRL format to comply with the regulations.

What are Taxes Payable? Taxes payable refers to one or more liability accounts that contain the current balance of taxes owed to government entities. Once these taxes are paid, they are removed from the taxes payable account with a debit. Income taxes payable. Payroll taxes payable.

Related Courses Bankruptcy Tax Guide Essentials of Corporate Bankruptcy What is the Liquidation Basis of Accounting? Liquidation basis accounting is concerned with preparing the financialstatements of a business in a different way if its liquidation is considered to be imminent.

Related Courses Business Ratios Guidebook Financial Analysis The Interpretation of FinancialStatements What is Net Profit Margin? If a company can apply a net operating loss carryforward to its before-tax profits, it can record a larger net profit margin. These expenses are known as discretionary expenses.

A change in cash flows is considered to be when there is a significant change in any one of the following (not including tax considerations): Risk A transaction can have commercial substance when there is risk , such as experiencing an increase in the risk that inbound cash flows will not occur as the result of a transaction.

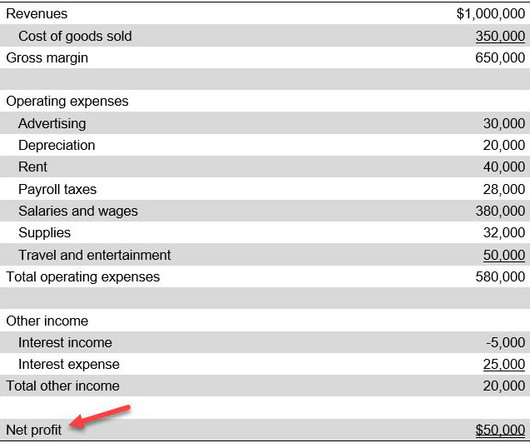

How to Calculate Net Profit To calculate net profit, subtract the cost of goods sold , operating expenses , financing costs, and tax costs from net revenues. The presentation appears in the following exhibit, which contains a sample income statement.

Related Courses Corporate Finance The Interpretation of FinancialStatements Treasurer's Guidebook What is Financial Leverage? Financial leverage is the use of debt to buy more assets. However, an excessive amount of financial leverage increases the risk of failure, since it becomes more difficult to repay debt.

An alternative way to calculate the cash flow of an entity is to add back all non-cash expenses (such as depreciation and amortization ) to its net after-tax profit, though this approach only approximates actual cash flows. This is one of the three financialstatements (the other two are the income statement and balance sheet ).

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content