This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

These systems can track income and expenses, generate financial reports, and integrate with other financial tools, ensuring accuracy and efficiency. Regularly Reconcile Accounts Reconciling accounts involves comparing financialrecords with bank statements to ensure they match.

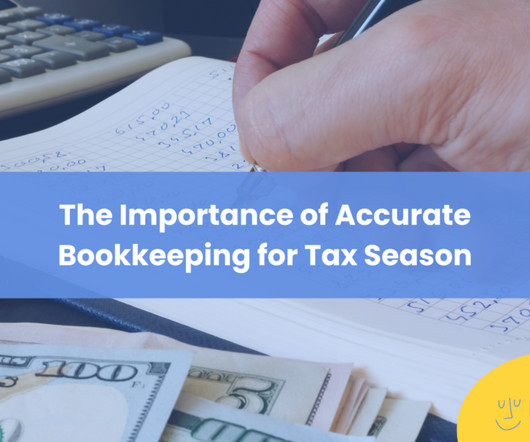

Among the various financial practices, record-keeping stands out as a fundamental aspect that cannot be overlooked. Accurate and consistent record-keeping is the backbone of any successful business, providing vital insights, facilitating compliance, aiding in decision-making, and fostering growth.

Understanding accrued revenue meaning is essential because it aligns a companys financialstatements with the business’s actual performance. It’s typically recognized in the financialstatements before an invoice is issued, following the accrual accounting principle.

This can occur if the income reported on your tax return does not match your business’s records and financialstatements. IRAS conducts thorough cross-checks, comparing the information you provide with other sources, like financialstatements and transactions, to ensure consistency and accuracy.

Traditional bookkeepers are professionals responsible for recordingfinancial transactions, maintaining ledgers, and preparing financialstatements manually or using basic accounting software. These professionals play a crucial role in ensuring the accuracy and integrity of a company's financialrecords.

In this blog, we will highlight a few key focus areas that will help you prepare for franchise audits and inspections, as well as emphasize the importance of prioritizing financial transparency and accountability for franchise owners. Compliance with Financial Reporting Standards. Tracking Revenue and Expenses.

This last-minute scramble typically involves gathering scattered receipts, invoices, and financialstatements, reconciling accounts, calculating tax obligations, and preparing financialstatements for tax filing.

Disbursements can occur in various contexts, including personal finance, business operations, government expenditures, and financial institutions like banks and investment firms. In business and financial contexts, disbursements are closely monitored to ensure that funds are allocated according to budgetary or contractual obligations.

The general ledger, in turn, is used to aggregate information into the financialstatements of a business; this can be done automatically with accounting software, or by manually compiling financialstatements from the information in a trial balance report (which is a summarization of the ending balances in the general ledger).

Books of original entry refers to the accounting journals in which business transactions are initially recorded. The information in these books is then summarized and posted into a general ledger , from which financialstatements are produced. This concept only applies to manual recordkeeping.

Year-End Small Business Accounting Checklist Prepare a closing schedule: Begin by creating a timeline highlighting key dates and deadlines, ensuring ample time for gathering necessary documents for accurate record-keeping. Doing so gives you a better understanding of your financial position so you can prepare for the year ahead.

It provides many benefits, including improved accuracy and efficiency in financialrecordkeeping. Some advantages of using software for bookkeeping include the following: Reduces manual tasks, such as uploading bank transactions, sending invoices, and reconciling ledgers. Track, reconcile, and manage inventory.

A rigorous bookkeeping process regularly reconciles accounts receivable balances with customer statements and payments. A quality bookkeeping process will regularly reconcile company credit card statements with internal expense records. Approval and authorization records. Credit card reconciliation.

If you’re like most marketing agencies, you’re probably more interested in creating compelling campaigns and generating leads than keeping track of your finances. But accurate record-keeping is essential to the success of any business. You might overspend or miss out on opportunities to grow your agency.

Either way, you’re better off keeping detailed records from day one. How do I keep proper records? What are financialstatements, and how do I get them? A single-person small business can get away with keeping written financialrecords in a notebook but large businesses need detailed entries.

Outsourcing bookkeeping services is the most cost-effective way for small businesses to get professional-grade financial reporting and bookkeeping without having to hire a dedicated in-house bookkeeper. Time and money savings Logging, recording, and organising financial data takes time and effort, especially if you do it manually.

Outsourcing bookkeeping services is the most cost-effective way for small businesses to get professional-grade financial reporting and bookkeeping without having to hire a dedicated in-house bookkeeper. Time and money savings Logging, recording, and organising financial data takes time and effort, especially if you do it manually.

Whether it's ensuring that expenses align with available funds or guaranteeing that business transactions accurately reflect the company's financial standing, tracking checks outstanding and reconciling bank statements is non-negotiable.

By reconciling invoices and payments promptly, businesses can avoid overpaying or missing payments, thereby maintaining healthy cash flow levels. This may involve contacting vendors, reviewing payment documentation, or reconcilingrecords with bank statements.

Try setting a goal for time spent on your bookkeeping tasks (choosing a specific time of day works well too) or a number of transactions/invoicing you want to reconcile. For example, if you have complex tax filings or financialstatements to prepare, it may be worth hiring a professional bookkeeper or accountant to help you.

Attention to Detail: Thoroughly record and reconcile all transactions to ensure accurate reporting and compliance. RecordKeeping: Keeping meticulous records of payroll, invoices, bank statements, and financialstatements is essential for monitoring your company’s financial health and compliance.

By implementing the right strategies and utilizing modern technologies, businesses can overcome these accounting hurdles and ensure a smoother financial flow. These errors can have a significant impact on financialstatements, leading to incorrect financial analysis and decision-making.

Discrepancies in Reported Wages Wage differences between your tax filings and payroll records often draw IRS attention. Reconcile your payroll, tax returns, and financialstatements on a regular basis. Organizing Payroll Records and Documentation Use a consistent system to store and access payroll documents.

Record-to-Report (R2R) is a critical finance management process in corporate finance, which focuses on collecting, processing, and delivering accurate financial data. For businesses, R2R is not merely a regulatory or accounting formality but serves as the backbone of strategic financial planning and analysis.

Integrations : Certain merchant account providers may integrate with your existing accounting and business management software, simplifying data entry and record-keeping. Depending on the provider you choose, you may need to provide other paperwork such as articles of incorporation and personal financial documents.

Understanding the distinctions between sales orders and invoices is crucial for accurate record-keeping and the smooth operation of a business. While sales orders may not always be recorded in accounting records, invoices should always be properly documented.

Here’s why it’s so crucial: Accurate FinancialRecords: Reconciliation ensures that financialrecords precisely mirror the actual expenses incurred. By cross-verifying records with spending, it minimizes errors in financialstatements, offering a more reliable picture of financial health.

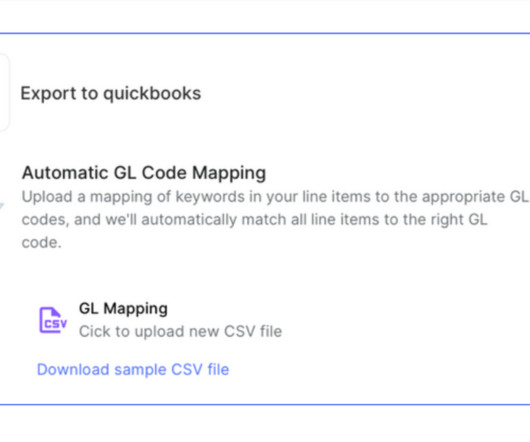

💡 The General Ledger Explained : At the heart of a company’s financialrecord-keeping lies the General Ledger (GL) – a comprehensive repository that records every financial transaction conducted by the business. For example, a business can assign a specific GL code to utility expenses.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content