This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The financial industry is experiencing a technological transformation that is reshaping accountsreceivable management. Financial and A/R teams are increasingly adopting automation, autonomous finance, machine learning, and artificial intelligence (AI) to enhance their workflows. Customizable reporting.

Skilled in all aspects of bookkeeping, including accounts payable/receivable, bank reconciliations, payroll processing, and financialreporting. Processed accounts payable and receivable, ensuring timely payments and collections. Reconciled bank statements monthly, maintaining accurate financial records.

For example, there might be a bucket for income received (sales), another for money spent on supplies (expenses), and accounts for things like cash on hand, money owed to you by customers (accountsreceivable), and money you owe to vendors (accounts payable).

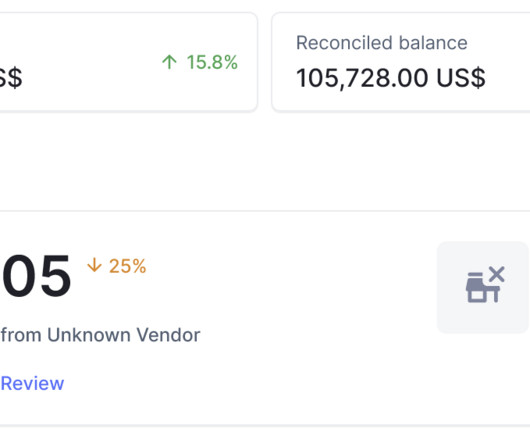

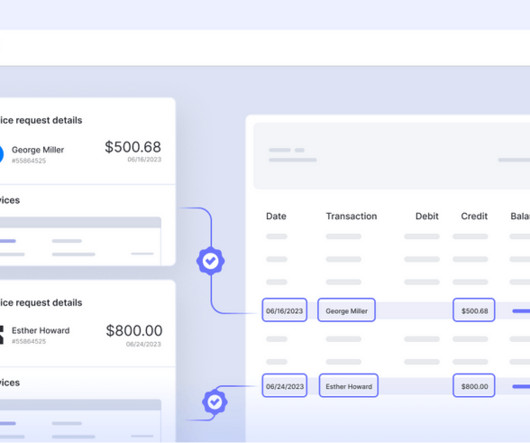

Accountsreceivable reconciliation is a crucial process within accounting and financial management practices undertaken regularly by a business. As transactions with customers and clients occur, businesses generate accountsreceivable, which represent amounts owed to them for goods and services sold or rendered.

In todays fast-paced business environment, achieving financial accuracy is critical for maintaining stakeholder trust and ensuring compliance with accounting standards. One cornerstone of accurate financialreporting is the matching principle in accounting, a concept that ensures revenues and expenses are recorded in the same period.

Technology has made it easier to track, categorize, and reconcilefinancial activity with far less effortand far fewer errors. Failing to Reconcile Bank and Credit Card Statements Reconciliation isnt just a formalityits how you ensure your books reflect your businesss reality.

It includes various accounts that track assets, liabilities, equity, revenue, and expenses. However, simply recording transactions in the general ledger is not sufficient to ensure accurate financialreporting. The process may vary depending on the complexity of the organization and the specific accounts being reconciled.

However, understanding basic bookkeeping terms will help you communicate with financial professionals and better understand your records. Pro Tip: Consult with a bookkeeper or accountant before choosing your methodswitching from cash to accrual (or vice versa) later can be a complicated process that may require IRS approval.

In most cases, you’ll find yourself delivering the product or service first, along with an invoice, and receiving payment later. This process is why an accountsreceivable (AR) ledger is your best friend. You may have made a sale, but the transaction isn’t complete until the money is in your bank account.

For businesses operating in dynamic industries, understanding the concept is essential for aligning with Generally Accepted Accounting Principles (GAAP) and maintaining transparency with stakeholders. We’ll also discuss best practices for recording it and why it’s critical for modern financial operations.

The traditional accountsreceivable process is full of manual processes that are prone to error. As a result, many businesses turn to accountsreceivable automation solutions. Make better credit decisions, lower DSO, and reconcile payments with near perfection. These key features include: Automated emails.

This direct connection means you always know exactly where you stand cash-wise – no reconciling or additional reports needed. Simpler bookkeeping and lower accounting costs Cash basis requires significantly less accounting expertise and time.

Its primary purpose is to ensure the accuracy and completeness of financial records so that financial statements can be prepared for internal and external reporting purposes. As part of the process, the AP team takes steps to ensure the past month’s financial records are accurate.

It will also give you a great picture of your business’s overall financial health. ReconcileAccounts You won’t get far if your books aren’t up to date. Take the time to reconcile bank statements, credit card statements, and any other financialaccounts.

Invest in accounting software or hire a professional bookkeeper to maintain organized and up-to-date records. Failure to Reconcile Bank Statements: Ignoring bank reconciliation is a recipe for disaster. Failing to reconcile your bank statements regularly can result in missed transactions, overdrafts, and errors in financialreporting.

Their responsibilities often include: Data Entry: Traditional bookkeepers manually record financial transactions, including sales, purchases, receipts, and payments, into ledgers or accounting software. Virtual bookkeepers with expertise in these industries can ensure compliance and accuracy in financialreporting.

However, with a shift towards Workflow Automation, application of AI is going beyond automating specific tasks but instead automating entire workflows including Accounts Payable, AccountsReceivable, Financial Close, FinancialReporting and Audits.

Today, accounting automation uses technology to, in many instances, completely remove the manual parts of an accountant’s work. Manually reconciling bank statements. Producing financialreports in a spreadsheet. Here’s an overview: 6) AccountsReceivable. Paying suppliers one-by-one.

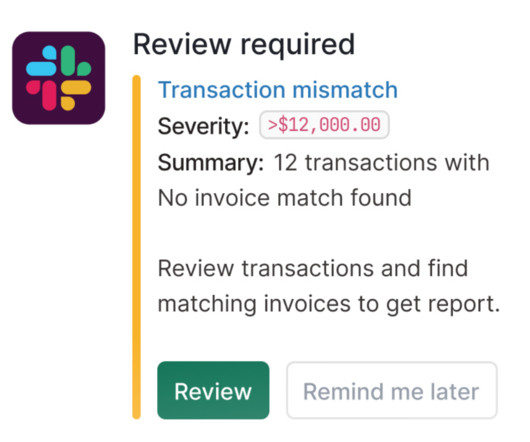

Discrepancies in your financialreports could lead to inaccurate data for future decisions, a mistake that could quickly spell disaster for any business. For this to happen, it must organize and perform account reconciliations for the period. However, this frequently doesn’t happen due to a lack of reconciling items.

Companies maintain various internal records to track their financial activities accurately and ensure compliance with accounting standards. Inventory Reconciliation : Inventory records are reconciled by comparing the quantities and values of inventory listed in the company's records with physical inventory counts.

The General Ledger is a central accounting record that contains all financial transactions of a business, organized in a systematic and structured manner. The GL comprises various accounts, each representing a specific financial aspect of the business.

Review and Approve: Validate reconciledaccounts for accuracy, seeking approval from stakeholders. Common Challenges and Discrepancies in the Account Reconciliation Process The Account Reconciliation process comes with its own set of challenges and potential discrepancies.

Some advantages of using software for bookkeeping include the following: Reduces manual tasks, such as uploading bank transactions, sending invoices, and reconciling ledgers. Run financialreports and data analytics easily. Track, reconcile, and manage inventory. Run payroll. Saves costs.

By doing regular balance sheet reconciliations, financial teams can address fraudulent activity, detect errors, and resolve discrepancies promptly. Accurate and timely financialreporting is important in maintaining trust with stakeholders and making informed business decisions.

Also, credit card reconciliation is the process of confirming that all transactions on your credit card statement are properly reflected in your accounting records. For businesses, credit card reconciliation ensures that all expenses are properly accounted for and reported. Why is reconciling credit cards difficult?

Matching and validating entries would mean data consolidation across sub-ledgers, vendor invoices, bank statements, receipts, and accountreceivables to ensure timely and accurate month-end and year-end closing of the financial books. Account Reconciliation can be a fairly manual task, especially right before the monthly close.

Our blogs regularly detail how professional bookkeeping can help businesses survive and thrive beyond simply recording transactions and preparing tax filings, like driving profitability with financialreporting , forecasting cash flow , and optimizing your accountsreceivable. Credit card reconciliation.

Cash management, accountsreceivable, prepaid expenses, fixed assets, accounts payable – there are countless activities that must be accounted for before closing the books for the month.

The role of payment reconciliation in maintaining financial accuracy is critical, as it helps businesses track their income, verify the legitimacy of transactions and prevent discrepancies. Accurate financial records are essential for businesses to meet auditing requirements and avoid potential fines or penalties for non-compliance.

Understanding the intricacies of bank reconciliation journal entries is essential for finance professionals and business owners alike, as it empowers them to identify, address, and prevent errors or discrepancies in financialreporting. Date Account Debited Account Credited Amount 12/21/23 Bank Charges Expense Cash $1000.00

By implementing the right strategies and utilizing modern technologies, businesses can overcome these accounting hurdles and ensure a smoother financial flow. Let's explore some common accounting problems and their solutions. Automation is key in streamlining various accounting tasks.

Efficient reconciliation of payments is a vital aspect of financial management for businesses of all sizes. As transactions flow in and out, reconciling payments becomes crucial to ensure accuracy, identify discrepancies, and maintain a clear financial picture. Why is payment reconciliation crucial for businesses?

Daily Accounting Tasks When work is piling up, it can be tempting to put off these day-to-day projects. However, these daily accounting tasks keep you organized, ensure your reporting remains accurate, and make audits much easier. Daily cash reconciliations create a paper trail and work as a control for the business.

How Does Account Reconciliation Work? How to ReconcileAccounts? The effectiveness of account reconciliation as an internal control measure is higher when the data being compared is from a third-party source, like a bank or credit card company. Furthermore, not all reconciling items necessitate adjustments to the balance.

The accuracy and reliability of financialreporting are vital for organizations to make informed decisions and meet regulatory requirements. To ensure the integrity of financial data, accountants and bookkeepers rely on the general ledger account reconciliation process. Sources: [link] [link] [link] 5.

It's a crucial step in the intercompany accounting process and for preparing a consolidated statement for financialreporting. This is essential for financialreporting and tax compliance. An account is considered reconciled when all the internal transactions can cancel out each other.

The Importance of Unbilled Revenue As unbilled receivables represent revenue that will eventually be recognized, its importance can be stressed enough with respect to financialreporting and analysis. Record the invoice: Using a journal entry, debit the unbilled receivablesaccount and credit the accountsreceivableaccount.

Ensure Compliance with Regulatory Standards Another important year-end task is verifying that all financialreporting complies with common accounting standards, such as Generally Accepted Accounting Principles (GAAP) and International FinancialReporting Standards (IFRS).

Settlement of an invoice refers to the process where the balance of an invoice is reconciled. When you receive an invoice for a product or service, you ensure that your payment matches the amount due. Your financial records should show this transaction correctly, marking the invoice as settled.

This can include cash, inventory, equipment, and accountsreceivable. Including loans, debt, accounts payable, and other expenses. Accounts Payable & AccountsReceivableAccounts payable is the amount of money your business owes to other businesses, suppliers, or vendors.

Businesses can skip this part by automating the entire invoice-to-cash workflow to streamline the accounts payable & accountsreceivable process and save time and resources. Moreover, an invoice automation solution reduces operational costs, helps staff reconcile purchase orders, and improves order-to-payment cycles.

The Importance of Expense Reconciliation Expense reconciliation holds significant importance in the realm of finance and accounting for several reasons: Financial Accuracy : One of the primary reasons for expense reconciliation is to ensure the accuracy of financial records.

In simple words, bookkeepers ensure that all of your business income, expenses and transactions are recorded in your book and they reconcile your company’s financialaccounts every month. In addition to that, bookkeepers can also help you prepare your company’s financial statement and financialreport.

Bookkeeper The bookkeeper position originates accounting transactions and compiles the information into financial statements. It also reconciles general ledger accounts. Controller The controller position manages the accounting department. Controller The controller position manages the accounting department.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content