This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Understanding how to account for cryptocurrency is critical. Since it behaves differently from traditional assets or cash, cryptocurrency should be treated as an intangible asset in your financialstatements. This can help automate transaction tracking and simplify financial recordkeeping.

Practical Tips for Maintaining Accurate Bookkeeping Implement a Reliable Bookkeeping System Investing in a reliable bookkeeping system is the foundation of accurate financialrecords. Small businesses can choose from various accountingsoftware options that automate and streamline bookkeeping tasks.

As a result, they are not bogged down by financialrecord-keeping tasks. The professional bookkeeping services cover everything from recordkeeping, bank reconciliations, and payroll management to tax preparation, financial reporting, and audit support.

Among the various financial practices, record-keeping stands out as a fundamental aspect that cannot be overlooked. Accurate and consistent record-keeping is the backbone of any successful business, providing vital insights, facilitating compliance, aiding in decision-making, and fostering growth.

Separate Business and Personal Finances One of the fundamental bookkeeping practices for freelancers is to keep personal and business finances separate. Open a separate bank account and credit card exclusively for business transactions.

Volume and Variety of Documents The Problem: The sheer volume of invoices, receipts, financialstatements and tax forms that need to be scanned, uploaded and filed can make this task overwhelming to start. Compatibility issues may arise, requiring custom solutions or additional investments in software and training.

Therefore, if the debit total and credit total on a trial balance do not match, this indicates that one or more transactions were recorded in the general ledger that were unbalanced. From a practical perspective, accountingsoftware packages do not allow users to enter unbalanced entries into the general ledger.

Here are just a few: Accountant: Accountants help organizations maintain their record-keeping, which may inform their financial decisions. You should receive your license in the mail within four to six weeks, although you might have access to a printable version earlier than that.

Establish a Solid Foundation with Accurate Record-Keeping The cornerstone of effective bookkeeping is meticulous record-keeping. Ensure every financial transaction is recorded accurately in your books. Utilizing accountingsoftware can streamline this process, reduce errors, and save time.

Traditional bookkeepers are professionals responsible for recordingfinancial transactions, maintaining ledgers, and preparing financialstatements manually or using basic accountingsoftware. What is Traditional Bookkeeping? Traditional bookkeepers typically work on-site.

Incorrect figures can affect a business’s ability to receive financial assistance, including timely loans. 2. Help during tax time Updated accounting and bookkeeping help with compliance during tax season. Catch-up is central to tax calculations and audited financialstatements.

These principles lay the foundation for accurate record-keeping and financial reporting. Double-entry bookkeeping : This principle states that every financial transaction should be recorded in at least two accounts, with equal debits and credits. Here are some key concepts about bookkeeping basics: 1.

The recordation process includes setting up a system of recordkeeping, tracking transactions within that system, and aggregating the resulting information into a set of financial reports. These three aspects of accounting are broken down into more detail below.

It also keeps people out of your personal accounts that you probably don’t want to be there. Accountingsoftware provides real-time insights, scalability and enhanced security measures compared to a manual process. Invoicing and Accounts Receivable Create an effective invoicing system to bill consumers quickly.

If you’re like most marketing agencies, you’re probably more interested in creating compelling campaigns and generating leads than keeping track of your finances. But accurate record-keeping is essential to the success of any business. You might overspend or miss out on opportunities to grow your agency.

They specialize in custom talent selection and training for accounting systems and excel in modern cloud accountingsoftware. Besides bookkeeping, they can handle other accounting tasks, with potential tax law training needed. Easily Adapt to Growth As your business grows, your accounting needs may become more complex.

The question here is: Have you laid the right financial foundation for your business? If not, start reviewing your financialstatements and see whether your business is poised for sustainable growth or one trembling on the edge? Use detailed cash flow statements to identify gaps and plan for smooth operations.

The general ledger, in turn, is used to aggregate information into the financialstatements of a business; this can be done automatically with accountingsoftware, or by manually compiling financialstatements from the information in a trial balance report (which is a summarization of the ending balances in the general ledger).

Record-to-Report (R2R) is a critical finance management process in corporate finance, which focuses on collecting, processing, and delivering accurate financial data. For businesses, R2R is not merely a regulatory or accounting formality but serves as the backbone of strategic financial planning and analysis.

A bookkeeper is a person responsible for handling a company’s financialrecords, ensuring accuracy and organization. These professionals record and enter every cost and revenue in a ledger or accountingsoftware. Feeling overwhelmed and making mistakes in financialrecords are clear indicators.

Either way, you’re better off keeping detailed records from day one. How do I keep proper records? What are financialstatements, and how do I get them? A single-person small business can get away with keeping written financialrecords in a notebook but large businesses need detailed entries.

Experience and Expertise : It is important to choose bookkeepers who have years of experience in handling financialstatement plans, budgeting and tax planning in small businesses. Use of AccountingSoftware : Make inquiries to find out if your bookkeeping service integrates business tools like payroll and CRM systems for efficiency.

While accountingsoftware has significantly helped businesses manage bookkeeping tasks, not every business can afford the subscriptions, let alone the cost of training and retaining a bookkeeper to enter and maintain data in the software. However, there are also potential drawbacks to consider when choosing bookkeeping software.

Think of it as the building block of your financialrecord-keeping system. It can help you detect and correct any errors in your books and provide the information you’ll need to demonstrate your business’s financial health to investors, lenders, and others.

Ways to Manage Your Business Accounting Outsource to Professionals: Leveraging specialised expertise through outsourcing can offer flexibility and cost-effectiveness. Using AccountingSoftware: Modern accountingsoftware empowers startups with small budgets to access functionalities for invoicing, expense tracking, and financial reporting.

When choosing an accounting firm , it's important to consider factors like industry experience , firm size , technology proficiency , communication, and reputation. Effective and efficient accounting strategies provide accurate financial information. Let's delve into each type: 1.

By implementing the right strategies and utilizing modern technologies, businesses can overcome these accounting hurdles and ensure a smoother financial flow. Let's explore some common accounting problems and their solutions. One of the major problems faced by businesses is material errors in financialstatements.

For example, if you have complex tax filings or financialstatements to prepare, it may be worth hiring a professional bookkeeper or accountant to help you. This involves streamlining your data entry and record-keeping, utilizing bookkeeping software and tools, and outsourcing your bookkeeping tasks when necessary.

After all, it just involves keeping a record of all the employees and their details such as their salaries, overtime hours, deductions, bonuses, holiday pay, taxes, etc. But payrolling doesn’t just involve keepingrecords. Ensuring compliance takes a lot of time, documentation, and expertise.

If you expect to need audited financialstatements in the future, use the accrual basis of accounting. Account Code Structure The account code structure is the numeric or alphanumeric designation given to each account in which information is stored.

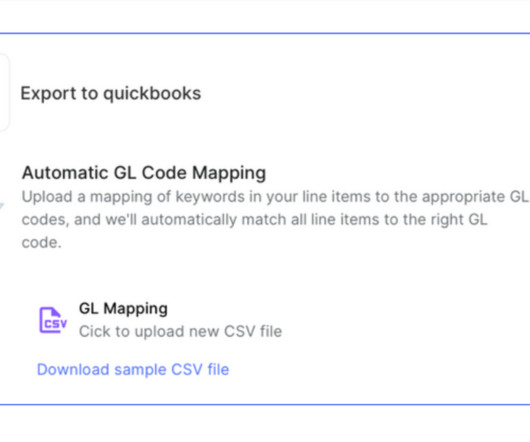

💡 The General Ledger Explained : At the heart of a company’s financialrecord-keeping lies the General Ledger (GL) – a comprehensive repository that records every financial transaction conducted by the business. For example, a business can assign a specific GL code to utility expenses.

During business tax preparation , choosing the standard deduction allows you to focus on running your business without worrying about extensive record-keeping. By itemizing deductions, businesses can ensure that every eligible expense is accounted for, maximizing the benefits.

Here’s why it’s so crucial: Accurate FinancialRecords: Reconciliation ensures that financialrecords precisely mirror the actual expenses incurred. By cross-verifying records with spending, it minimizes errors in financialstatements, offering a more reliable picture of financial health.

This amount will be marked as "accounts receivable" until the client pays the invoice. Once the payment is received, the accounts receivable will be recorded as "cash" or "revenue" on the company's financialstatements. The account is written off as bad debt if payment is not received.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content