This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

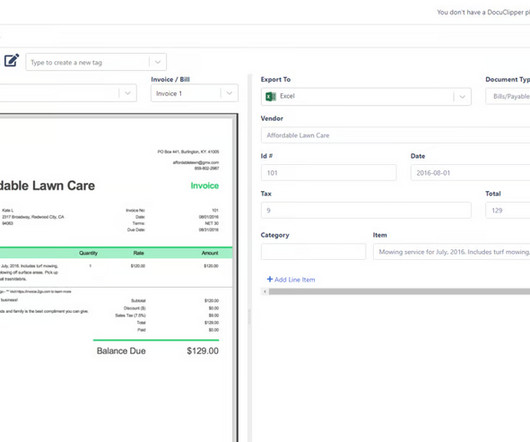

DocuClipper is an OCR-powered financial document processing tool that converts bank statements, credit card statements, invoices, receipts, and brokerage statements into Excel, CSV, or accounting software-ready formats. AutoEntry Automated dataentry for accounting No Yes Ease of use, accounting integration SMBs, accounting firms 3.8

AI-powered automation Number-crunching and manual dataentry that used to take hours are now handled in seconds by AI. From categorizing expenses to reconciling accounts and forecasting trends, artificial intelligence does the heavy lifting at scale and without human error. That’s where client portals come in.

You may often need to integrate Salesforce and NetSuite to avoid easier dataentry, streamline manual processes, and enable real-time insights into sales and finance data. Improved Efficiency : Your operations team ends up saving hours spent on manual dataentry.

Connecting your systems directly: Reduces manual dataentry and errors Ensures automatic syncing of sales transactions Helps track platform-specific fees and commissions 3. Regularly Reconcile Transactions Reconciling sales data with bank statements and payment processors prevents discrepancies.

Relying on Manual Processes for Bookkeeping Tasks Manual dataentry might seem manageable when youre just starting, but it quickly becomes inefficient and risky as your business grows. Technology has made it easier to track, categorize, and reconcile financial activity with far less effortand far fewer errors.

For instance, sales from Europe can be VAT subject to documentation even when the seller is not paying it directly. The best eCommerce accounting services reconcile your platform payments with real-life bank deposits and expenditures. Your accountant for eCommerce business does dataentry, categorization, and financial reporting.

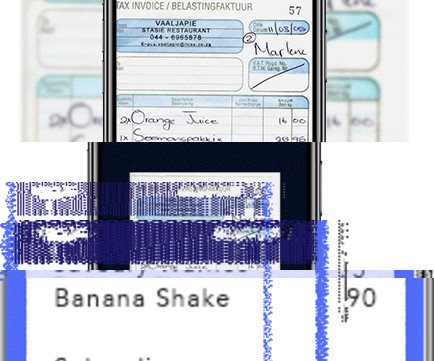

A business bank statement is an official document provided by your bank that summarizes all the transactions in your business account over a specific period. This document includes details such as deposits, withdrawals, interest earned, and any fees charged.

Otherwise, you may be able to enter expense data into an AI model directly with some context and explanations for your expense categories to automate classification and generate expense reports more quickly. Reconciling Accounts AI tools can help accountants work more efficiently.

Your accounting team will track deductions throughout the year, maintain organized documentation, and implement tax planning strategies to optimize your position. They can design an integrated technology ecosystem that reduces manual dataentry, minimizes errors, and provides real-time financial visibility.

We are forced to manually enter data, reconcile transactions, and sift through files trying to locate financial information we need. The AI validates extracted data against existing records, flagging any discrepancies that need human attention. The AI also sorts the uploaded document automatically.

A documented case from an accounting journal described a small business that, despite having books that satisfied tax requirements, failed because its records offered no actionable insight for management. The lack of reliable cost information led to bad bids and shrinking profits, ultimately resulting in closure.

Furthermore, manual dataentry drained hours. This level of automation helps keep everyone informed while reducing the time you spend compiling documents. AI accounting software gives you access to real-time financial data on your phone, tablet, or laptop. Mistakes were common.

From collecting documents to automating government obligations, it takes the manual hassle out of the process. Integrating seamlessly with Xero payroll, this app captures accurate work hours, breaks, and even job costing data. These apps can be particularly handy for businesses with diverse teams or complex scheduling.

This means you can reconcile multiple records faster while minimising errors in manual dataentry. Make sure your advisor knows that you’re using the file library so they can also find and share documents. EOFY 2023).

The efficiency in organizing financial documents, such as tax records, invoices, receipts, bank statements, and reports can make a significant difference on their own efficiency and success and the organization’s compliance. Canadians are required to store documents relating to their tax return for at least 6 years incase of an audit.

Paperless document management allows you to upload, store, and manage your financial documents in one central location. With LedgerDocs, you can easily upload receipts, invoices, and other financial documents by scanning them or taking a picture with your smartphone. Saves time and reduces errors.

Gone are the days of tedious manual dataentry and stacks of paper ledgers. Their responsibilities often include: DataEntry: Traditional bookkeepers manually record financial transactions, including sales, purchases, receipts, and payments, into ledgers or accounting software.

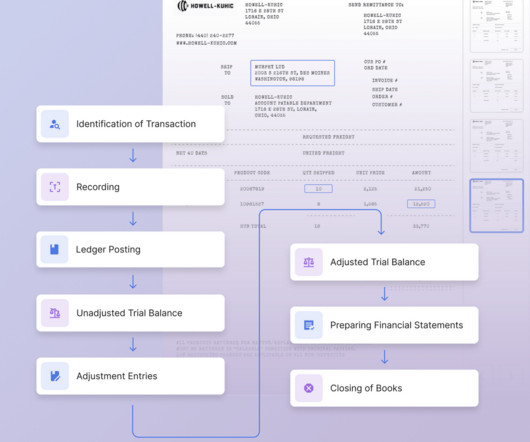

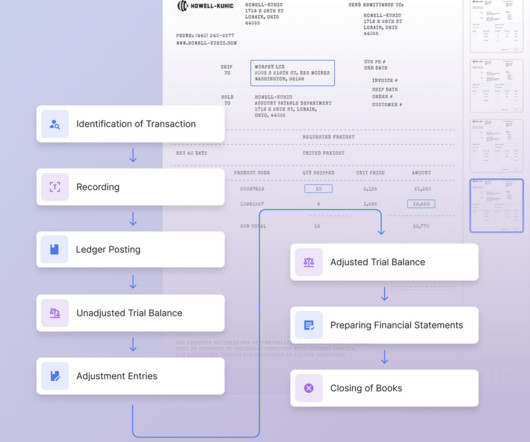

The process involves a series of steps and tasks that are designed to reconcile financial accounts, verify transactions, and produce accurate financial statements. For example, they may reconcile vendor statements with the AP ledger to ensure there are no discrepancies or missed invoices.

Using our app on your smartphone, you can snap a picture of any expense receipt, add any notes or tags, for your bookkeeper’s reference, directly to the receipt, categorize the receipt, and upload it onto the document management platform. Saving yourself hours a month of manual dataentry.

Why is it Important to Reconcile your Bank Account? Reconciling the bank statement involves comparing the company's internal financial records or ledger to the bank statement received via the bank. How Often Should You Reconcile Your Bank Statements? They can benefit by reconciling their bank statements monthly.

Doing so can simplify time-consuming tasks like posting invoices, recording payments, reconciling balances, and managing disputed invoices. The integration also enables two-way data synchronization to ensure exactly the same information is available on both systems. Properly Document and Test all Integrations.

Using our app on your smartphone, you can snap a picture of any expense receipt, add any notes or tags, for your bookkeeper’s reference, directly to the receipt, categorize the receipt, and upload it onto the document management platform. Saving yourself hours a month of manual dataentry.

These tasks include dataentry, invoice processing, and financial analysis for decision-making, operational planning, and risk management. Manual dataentry implies there is a high potential for inaccuracies, as human errors can occur when transcribing numbers or processing large volumes of data.

Whether you are a small business or a large enterprise, reconciling invoices is an essential process to ensure accuracy, identify discrepancies, and maintain strong financial controls. Client and partner retention Accurate and reconciled numbers are essential for building and maintaining solid relationships with vendors and suppliers.

Balance sheet reconciliation is a critical financial process that aligns the financial statements with external documentation such as bank statements, invoices, and general ledger entries. Finance teams can also follow specific templates designed to reconcile their balance sheets manually. What is Balance Sheet Reconciliation?

At the core of accounts management lies account reconciliation, the process of comparing various financial documents to ensure accuracy and accountability. Document Process: Maintain detailed records of steps, findings, and adjustments. Investigate Discrepancies: Analyze differences, trace transactions and rectify errors.

It involves comparing and reconciling the balances of various accounts in the balance sheet with supporting documentation. It involves comparing the balances of various accounts listed in the balance sheet to external documentation, such as bank statements and general ledger entries. How to reconcile balance sheets?

Matching and validating entries would mean data consolidation across sub-ledgers, vendor invoices, bank statements, receipts, and account receivables to ensure timely and accurate month-end and year-end closing of the financial books. Account Reconciliation can be a fairly manual task, especially right before the monthly close.

However, the rise in credit card usage has led to financial nightmares across accounting teams at the end of the month because this means the transactions that need to be reconciled are also on the rise. This results in a gap in the documentation and invoices are involved to fill in the gap by matching against the credit card statements.

However, the GL is not the sole repository of financial data. Businesses maintain a multitude of other financial documents, including bank statements, invoices , bills, cash payment receipts, and more. What is the General Ledger? What is General Ledger Reconciliation and What are Its Types?

Accounts payable teams must reconcile payments regularly to avoid double-processing them. The process involves matching the amounts that your vendors bill and comparing them to the company's accounts payable documents. Errors in logging payments correctly, duplicates, or missing entries may lead to incorrect reporting.

This process typically involves reviewing transactions, invoices, receipts, and other financial documents to verify that they match up with the company's records and budget. By reconciling expenses, businesses can ensure that they comply with these regulations and avoid potential penalties or legal issues.

Xero’s software handles accounts payable as a traditional system requiring manual dataentry. Then accounts payable routes the matched (often paper-based) documents to the right approver and follows up with approvers when their approval isn’t timely. The Xero company, founded in 2006, is New Zealand-based.

Once the check is cashed, its reconciled with the invoice 9. The invoice and all related documentation are filed While the specifics of the accounts payable process may vary at different organizations, its essence is similar the AP team processes invoices and issues payments. Document storage Physical space for filing cabinets.

Reconciling invoices typically involves someone manually spending hours browsing through several invoices and jotting things down in a ledger. Invoice OCR refers to the process of extracting relevant data from scanned or PDF invoices and converting it into a machine readable format that is both editable and searchable.

General ledger reconciliation is a fundamental accounting practice that verifies the consistency and accuracy of account balances, identifies discrepancies, and ensures the financial data aligns with the underlying transactions. The process may vary depending on the complexity of the organization and the specific accounts being reconciled.

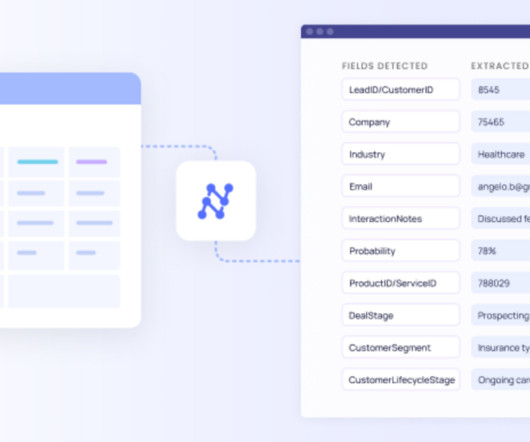

With advanced OCR and AI-powered data extraction, Nanonets enables enterprises to capture data from documents accurately, regardless of the format. Nanonets stand out with the following key features: The AI-powered OCR technology accurately captures invoice data from any format, reducing manual dataentry by up to 95%.

However, let's understand the manual bank reconciliation process once: Step 1: Gather documents On the bank side, you need the bank statements, outstanding checks, deposits, and any pending transactions. If they match, it means your records and the bank statement are reconciled, and there are no discrepancies.

However, let's understand the manual bank reconciliation process once: Step 1: Gather documents On the bank side, you need the bank statements, outstanding checks, deposits, and any pending transactions. If they match, it means your records and the bank statement are reconciled, and there are no discrepancies.

Vendor reconciliation , a crucial part of this process, involves scrutinizing purchase-related documents to ensure accuracy in all vendor transactions. " Reconciliation in accounting refers to the comparing of details of transactions and financial activities between various documents.

One method involves a thorough review of documents and transactions to verify their accuracy and consistency with bank statements. The bank reconciliation process involves several steps: Gathering Necessary Documents: Collecting bank statements, checkbooks, deposit slips, and invoices, bills, and receipts for comparison.

Want automated data extraction capabilities once you upload your documents (meaning no dataentry or creating templates) and transaction matching powered by ML algorithms (meaning AI matching) across documents you either upload, receive from an email or provide connection to the database ? Use CubeSoftware.

As transactions flow in and out, reconciling payments becomes crucial to ensure accuracy, identify discrepancies, and maintain a clear financial picture. This article will provide a comprehensive guide to reconciling payments, its importance, challenges faced, best practices, and the role of automation in enhancing the process.

This means no more: Manual dataentry into a computer. Manually reconciling bank statements. Chasing after documents from your client. elimination of manual accounting dataentry and human error). The extracted financial data syncs with your cloud accounting software. Paying suppliers one-by-one.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content