This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

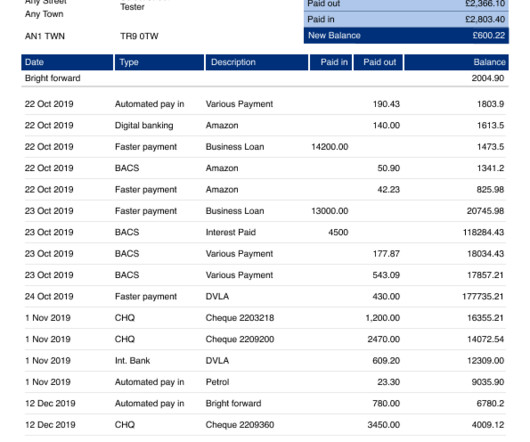

Bank Reconciliation Process Flow The essential process flow for a bank reconciliation is to start with the bank's ending cash balance, add to it any deposits in transit from the company to the bank, subtract any checks that have not yet cleared the bank, and either add or deduct any other items. Outstanding check.

Challenge 4: Lack Of Integration Options Trying to sync invoicing data with your accountingsoftware manually takes a lot of work. Solution Automated invoicing tools integrate seamlessly with accountingsoftware like QuickBooks, Xero, and PayPal, so your financial data stays up-to-date with minimal effort.

A bank reconciliation statement is a form used to compare internal records of checking account activity to those stated by the bank. It itemizes the deposits, withdrawals, and other activities impacting the checking account for a one-month period. Add the total of all deposits in transit to the bank.

In a survey, 58% of accountants said automated accounting led to increased efficiency. US accounting services show that nearly 75% of accounting tasks can be automated. This could explain the high growth of the accountingsoftware industry, estimated to reach $12 billion by 2026.

Establishing a record-keeping system for tracking income and expenses is essential. Choosing the right bookkeeping software with features such as invoicing options and integration with bank accounts is important. First and foremost, you need to establish a recordkeeping system to maintain accurate financial records.

Unrecorded Transactions : Failure to record all transactions, such as outstanding checks or pending deposits, can lead to discrepancies in reconciled accounts. It's essential to ensure that all transactions are accurately recorded and accounted for.

Real-Time Tracking: Keep tabs on the status of your invoices. Integration With AccountingSoftware: Easily integrate your invoicing software with accounting tools for better financial management and transparency. Sage Sage stands as a stalwart in the accountingsoftware arena. What’s Exceptional?

In this blog, we will explore the essential task of filling out receipt books, a foundational element of financial record-keeping for both small and large businesses. We will also delve into the benefits of automating your receipt books and how platforms like Nanonets can transform your approach to financial record-keeping.

💡 Bank statement verification is the process of confirming that the details in a bank statement—such as deposits, withdrawals, and balances—are accurate and authentic. Blockchain technology: Some verification systems adopt blockchain for secure, tamper-proof record-keeping.

Approval workflow is integrated into the company's expense management software for tracking and record-keeping. Digital RecordKeeping: With OCR, digital copies of receipts can be stored efficiently, making it easier to retrieve documents for audits or compliance checks. bi-weekly, monthly) and stick to it.

Merchant accounts: A type of bank account that allows businesses to accept and process electronic payments. Merchant accounts act as intermediary holding accounts where funds are deposited after transactions are approved but before funds are transferred to the supplier’s bank account.

Features: Flexible intake and approval workflows, Seamless integration with other business systems and with general ledgers, Creation of rules that reflect the company’s specific policies Recordkeeping of every dollar spent Easy retrieval of documentation for auditing or booking purposes.

Once the payment is received, the accounts receivable will be recorded as "cash" or "revenue" on the company's financial statements. Different bookkeepers and accountingsoftware programs may use different terms for accounts receivable, but the concept is always the same.

This is where many businesses stumble, struggling to keep up with ever-changing regulations and internal policies. In a world where your expense management system needs to talk to your accountingsoftware, your ERP system, and maybe even your CRM, integration is key. And let's not forget about integration issues.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content